Related Research Articles

Financial economics is the branch of economics characterized by a "concentration on monetary activities", in which "money of one type or another is likely to appear on both sides of a trade". Its concern is thus the interrelation of financial variables, such as share prices, interest rates and exchange rates, as opposed to those concerning the real economy. It has two main areas of focus: asset pricing and corporate finance; the first being the perspective of providers of capital, i.e. investors, and the second of users of capital. It thus provides the theoretical underpinning for much of finance.

In finance, a futures contract is a standardized legal contract to buy or sell something at a predetermined price for delivery at a specified time in the future, between parties not yet known to each other. The item transacted is usually a commodity or financial instrument. The predetermined price of the contract is known as the forward price or delivery price. The specified time in the future when delivery and payment occur is known as the delivery date. Because it derives its value from the value of the underlying asset, a futures contract is a derivative.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

Volatility risk is the risk of an adverse change of price, due to changes in the volatility of a factor affecting that price. It usually applies to derivative instruments, and their portfolios, where the volatility of the underlying asset is a major influencer of option prices. It is also relevant to portfolios of basic assets, and to foreign currency trading.

In finance, the beta is a statistic that measures the expected increase or decrease of an individual stock price in proportion to movements of the stock market as a whole. Beta can be used to indicate the contribution of an individual asset to the market risk of a portfolio when it is added in small quantity. It refers to an asset's non-diversifiable risk, systematic risk, or market risk. Beta is not a measure of idiosyncratic risk.

A quanto is a type of derivative in which the underlying is denominated in one currency, but the instrument itself is settled in another currency at some rate. Such products are attractive for speculators and investors who wish to have exposure to a foreign asset, but without the corresponding exchange rate risk.

The Tokyo Commodity Exchange, or TOCOM, is an energy exchange in Tokyo, Japan. TOCOM is operated by Tokyo Commodity Exchange, Inc., a wholly owned subsidiary of Japan Exchange Group (JPX). Under the Commodity Derivatives Transaction Act of Japan, It is a licensed commodity exchange operator that provides market facilities for trading of commodity derivatives, physical commodities and commodity price index futures.

In financial economics, asset pricing refers to a formal treatment and development of two interrelated pricing principles, outlined below, together with the resultant models. There have been many models developed for different situations, but correspondingly, these stem from either general equilibrium asset pricing or rational asset pricing, the latter corresponding to risk neutral pricing.

Financial risk is any of various types of risk associated with financing, including financial transactions that include company loans in risk of default. Often it is understood to include only downside risk, meaning the potential for financial loss and uncertainty about its extent.

The bullwhip effect is a supply chain phenomenon where orders to suppliers tend to have a larger variability than sales to buyers, which results in an amplified demand variability upstream. In part, this results in increasing swings in inventory in response to shifts in consumer demand as one moves further up the supply chain. The concept first appeared in Jay Forrester's Industrial Dynamics (1961) and thus it is also known as the Forrester effect. It has been described as "the observed propensity for material orders to be more variable than demand signals and for this variability to increase the further upstream a company is in a supply chain". Research at Stanford University helped incorporate the concept into supply chain vernacular using a story about Volvo. Suffering a glut in green cars, sales and marketing developed a program to sell the excess inventory. While successful in generating the desired market pull, manufacturing did not know about the promotional plans. Instead, they read the increase in sales as an indication of growing demand for green cars and ramped up production.

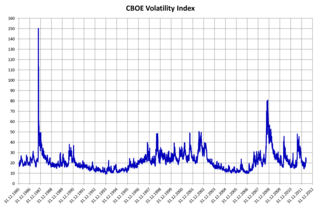

VIX is the ticker symbol and the popular name for the Chicago Board Options Exchange's CBOE Volatility Index, a popular measure of the stock market's expectation of volatility based on S&P 500 index options. It is calculated and disseminated on a real-time basis by the CBOE, and is often referred to as the fear index or fear gauge.

Foreign exchange risk is a financial risk that exists when a financial transaction is denominated in a currency other than the domestic currency of the company. The exchange risk arises when there is a risk of an unfavourable change in exchange rate between the domestic currency and the denominated currency before the date when the transaction is completed.

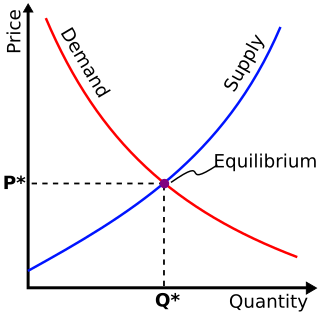

In economics, demand is the quantity of a good that consumers are willing and able to purchase at various prices during a given time. In economics "demand" for a commodity is not the same thing as "desire" for it. It refers to both the desire to purchase and the ability to pay for a commodity.

The following outline is provided as an overview of and topical guide to finance:

Revenue management (RM) is a discipline to maximize profit by optimizing rate (ADR) and occupancy (Occ). In its day to day application the maximization of Revenue per Available Room (RevPAR) is paramount. It is seen by some as synonymous with yield management.

In finance, volatility is the degree of variation of a trading price series over time, usually measured by the standard deviation of logarithmic returns.

Weather risk management is a type of risk management done by organizations to address potential financial losses caused by unusual weather.

Electricity pricing can vary widely by country or by locality within a country. Electricity prices are dependent on many factors, such as the price of power generation, government taxes or subsidies, CO

2 taxes, local weather patterns, transmission and distribution infrastructure, and multi-tiered industry regulation. The pricing or tariffs can also differ depending on the customer-base, typically by residential, commercial, and industrial connections.

Channel coordination aims at improving supply chain performance by aligning the plans and the objectives of individual enterprises. It usually focuses on inventory management and ordering decisions in distributed inter-company settings. Channel coordination models may involve multi-echelon inventory theory, multiple decision makers, asymmetric information, as well as recent paradigms of manufacturing, such as mass customization, short product life-cycles, outsourcing and delayed differentiation. The theoretical foundations of the coordination are based chiefly on the contract theory. The problem of channel coordination was first modeled and analyzed by Anantasubramania Kumar in 1992.

Energy forecasting includes forecasting demand (load) and price of electricity, fossil fuels and renewable energy sources. Forecasting can be both expected price value and probabilistic forecasting.

References

- 1 2 3 Volume Risk, openriskmanual.org

- 1 2 3 Volume Risk, capital.com

- ↑ Kandl, Peter; Studer, Gerold (January 2001). "Factoring in volume risk". Risk Magazine: 84f. Retrieved 23 October 2015.

- ↑ Pellegrino, R.; Tauro, D. (March 27, 2018). "Supply Chain Finance: A supply chain-oriented perspective to mitigate commodity risk and pricing volatility (in press)". Journal of Purchasing and Supply Management . doi:10.1016/j.pursup.2018.03.004. S2CID 169679135.

- 1 2 Volume Risk and Price Risk, TAS Royalty Company

- ↑ Revenue Risk, APM Group

- ↑ Jay Ogilvy (2015). "Scenario Planning and Strategic Forecasting", forbes.com

- ↑ International Monetary Fund (2019). "PPP Fiscal Risk Assessment Model"

- ↑ Global Infrastructure Hub (2016). "Allocating Risks in Public-Private Partnership Contracts"

- 1 2 3 Yumi Oum, Shmuel Oren, Shijie Deng (2006). "Hedging Quantity Risks with Standard Power Options in a Competitive Wholesale Electricity Market". Naval Research Logistics. Vol. 53.

- ↑ Takuji Matsumoto, Yuji Yamada (2021). "Simultaneous hedging strategy for price and volume risks in electricity businesses using energy and weather derivatives". Energy Economics. Volume 95, March 2021

- ↑ Bloomberg.com (2022). 5 things new commodities hedgers need to know

| | This finance-related article is a stub. You can help Wikipedia by expanding it. |