In finance, a bond is a type of security under which the issuer (debtor) owes the holder (creditor) a debt, and is obliged – depending on the terms – to provide cash flow to the creditor. The timing and the amount of cash flow provided varies, depending on the economic value that is emphasized upon, thus giving rise to different types of bonds. The interest is usually payable at fixed intervals: semiannual, annual, and less often at other periods. Thus, a bond is a form of loan or IOU. Bonds provide the borrower with external funds to finance long-term investments or, in the case of government bonds, to finance current expenditure.

A government bond or sovereign bond is a form of bond issued by a government to support public spending. It generally includes a commitment to pay periodic interest, called coupon payments, and to repay the face value on the maturity date.

In finance, a convertible bond, convertible note, or convertible debt is a type of bond that the holder can convert into a specified number of shares of common stock in the issuing company or cash of equal value. It is a hybrid security with debt- and equity-like features. It originated in the mid-19th century, and was used by early speculators such as Jacob Little and Daniel Drew to counter market cornering.

In finance, the yield on a security is a measure of the ex-ante return to a holder of the security. It is one component of return on an investment, the other component being the change in the market price of the security. It is a measure applied to fixed income securities, common stocks, preferred stocks, convertible stocks and bonds, annuities and real estate investments.

United States Treasury securities, also called Treasuries or Treasurys, are government debt instruments issued by the United States Department of the Treasury to finance government spending, in addition to taxation. Since 2012, the U.S. government debt has been managed by the Bureau of the Fiscal Service, succeeding the Bureau of the Public Debt.

The yield to maturity (YTM), book yield or redemption yield of a fixed-interest security is an estimate of the total rate of return anticipated to be earned by an investor who buys it at a given market price, holds it to maturity, and receives all interest payments and the capital redemption on schedule.

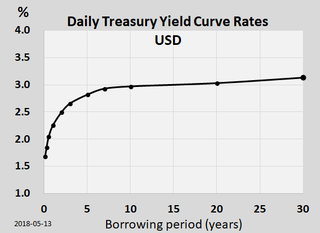

In finance, the yield curve is a graph which depicts how the yields on debt instruments – such as bonds – vary as a function of their years remaining to maturity. Typically, the graph's horizontal or x-axis is a time line of months or years remaining to maturity, with the shortest maturity on the left and progressively longer time periods on the right. The vertical or y-axis depicts the annualized yield to maturity.

Fixed income refers to any type of investment under which the borrower or issuer is obliged to make payments of a fixed amount on a fixed schedule. For example, the borrower may have to pay interest at a fixed rate once a year and repay the principal amount on maturity. Fixed-income securities can be contrasted with equity securities that create no obligation to pay dividends or any other form of income. Bonds carry a level of legal protections for investors that equity securities do not: in the event of a bankruptcy, bond holders would be repaid after liquidation of assets, whereas shareholders with stock often receive nothing.

Bond valuation is the process by which an investor arrives at an estimate of the theoretical fair value, or intrinsic worth, of a bond. As with any security or capital investment, the theoretical fair value of a bond is the present value of the stream of cash flows it is expected to generate. Hence, the value of a bond is obtained by discounting the bond's expected cash flows to the present using an appropriate discount rate.

In finance, bond convexity is a measure of the non-linear relationship of bond prices to changes in interest rates, and is defined as the second derivative of the price of the bond with respect to interest rates. In general, the higher the duration, the more sensitive the bond price is to the change in interest rates. Bond convexity is one of the most basic and widely used forms of convexity in finance. Convexity was based on the work of Hon-Fei Lai and popularized by Stanley Diller.

The current yield, interest yield, income yield, flat yield, market yield, mark to market yield or running yield is a financial term used in reference to bonds and other fixed-interest securities such as gilts. It is the ratio of the annual interest (coupon) payment and the bond's price:

Floating rate notes (FRNs) are bonds that have a variable coupon, equal to a money market reference rate, like SOFR or federal funds rate, plus a quoted spread. The spread is a rate that remains constant. Almost all FRNs have quarterly coupons, i.e. they pay out interest every three months. At the beginning of each coupon period, the coupon is calculated by taking the fixing of the reference rate for that day and adding the spread. A typical coupon would look like 3 months USD SOFR +0.20%.

A mortgage-backed security (MBS) is a type of asset-backed security which is secured by a mortgage or collection of mortgages. The mortgages are aggregated and sold to a group of individuals that securitizes, or packages, the loans together into a security that investors can buy. Bonds securitizing mortgages are usually treated as a separate class, termed residential; another class is commercial, depending on whether the underlying asset is mortgages owned by borrowers or assets for commercial purposes ranging from office space to multi-dwelling buildings.

A convertible security is a financial instrument whose holder has the right to convert it into another security of the same issuer. Most convertible securities are convertible bonds or preferred stocks that pay regular interest and can be converted into shares of the issuer's common stock. Convertible securities typically include other embedded options, such as call or put options. Consequently, determining the value of convertible securities can be a complex exercise. The complex valuation issue may attract specialized professional investors, including arbitrageurs and hedge funds who try to exploit disparities in the relationship between the price of the convertible security and the underlying common stock.

A corporate bond is a bond issued by a corporation in order to raise financing for a variety of reasons such as to ongoing operations, mergers & acquisitions, or to expand business. It is a longer-term debt instrument indicating that a corporation has borrowed a certain amount of money and promises to repay it in the future under specific terms. Corporate debt instruments with maturity shorter than one year are referred to as commercial paper.

In finance, interest rate immunization is a portfolio management strategy designed to take advantage of the offsetting effects of interest rate risk and reinvestment risk.

Fixed-income arbitrage is a group of market-neutral-investment strategies that are designed to take advantage of differences in interest rates between varying fixed-income securities or contracts. Arbitrage in terms of investment strategy, involves buying securities on one market for immediate resale on another market in order to profit from a price discrepancy.

Reinvestment risk is a form of financial risk. It is primarily associated with fixed income securities, in the form of early redemption risk and coupon reinvestment risk.

The Z-spread, ZSPRD, zero-volatility spread, or yield curve spread of a bond is the parallel shift or spread over the zero-coupon Treasury yield curve required for discounting a predetermined cash flow schedule to arrive at its present market price. The Z-spread is also widely used in the credit default swap (CDS) market as a measure of credit spread that is relatively insensitive to the particulars of specific corporate or government bonds.

In finance, par yield is the yield on a fixed income security assuming that its market price is equal to par value. Par yield is used to derive the U.S. Treasury’s daily official “Treasury Par Yield Curve Rates”, which are used by investors to price debt securities traded in public markets, and by lenders to set interest rates on many other types of debt, including bank loans and mortgages.