Related Research Articles

A security is a tradable financial asset. The term commonly refers to any form of financial instrument, but its legal definition varies by jurisdiction. In some countries and languages people commonly use the term "security" to refer to any form of financial instrument, even though the underlying legal and regulatory regime may not have such a broad definition. In some jurisdictions the term specifically excludes financial instruments other than equities and fixed income instruments. In some jurisdictions it includes some instruments that are close to equities and fixed income, e.g., equity warrants.

In finance, a bond is a type of security under which the issuer (debtor) owes the holder (creditor) a debt, and is obliged – depending on the terms – to provide cash flow to the creditor. The timing and the amount of cash flow provided varies, depending on the economic value that is emphasized upon, thus giving rise to different types of bonds. The interest is usually payable at fixed intervals: semiannual, annual, and less often at other periods. Thus, a bond is a form of loan or IOU. Bonds provide the borrower with external funds to finance long-term investments or, in the case of government bonds, to finance current expenditure.

In corporate finance, a debenture is a medium- to long-term debt instrument used by large companies to borrow money, at a fixed rate of interest. The legal term "debenture" originally referred to a document that either creates a debt or acknowledges it, but in some countries the term is now used interchangeably with bond, loan stock or note. A debenture is thus like a certificate of loan or a loan bond evidencing the company's liability to pay a specified amount with interest. Although the money raised by the debentures becomes a part of the company's capital structure, it does not become share capital. Senior debentures get paid before subordinate debentures, and there are varying rates of risk and payoff for these categories.

The money market is a component of the economy that provides short-term funds. The money market deals in short-term loans, generally for a period of a year or less.

In finance, a convertible bond, convertible note, or convertible debt is a type of bond that the holder can convert into a specified number of shares of common stock in the issuing company or cash of equal value. It is a hybrid security with debt- and equity-like features. It originated in the mid-19th century, and was used by early speculators such as Jacob Little and Daniel Drew to counter market cornering.

In finance, the yield on a security is a measure of the ex-ante return to a holder of the security. It is one component of return on an investment, the other component being the change in the market price of the security. It is a measure applied to fixed income securities, common stocks, preferred stocks, convertible stocks and bonds, annuities and real estate investments.

United States Treasury securities, also called Treasuries or Treasurys, are government debt instruments issued by the United States Department of the Treasury to finance government spending in addition to taxation. Since 2012, U.S. government debt has been managed by the Bureau of the Fiscal Service, succeeding the Bureau of the Public Debt.

Preferred stock is a component of share capital that may have any combination of features not possessed by common stock, including properties of both an equity and a debt instrument, and is generally considered a hybrid instrument. Preferred stocks are senior to common stock but subordinate to bonds in terms of claim and may have priority over common stock in the payment of dividends and upon liquidation. Terms of the preferred stock are described in the issuing company's articles of association or articles of incorporation.

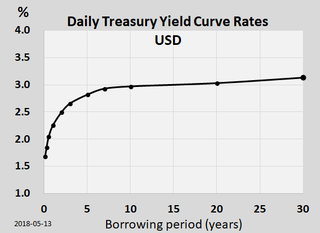

In finance, the yield curve is a graph which depicts how the yields on debt instruments – such as bonds – vary as a function of their years remaining to maturity. Typically, the graph's horizontal or x-axis is a time line of months or years remaining to maturity, with the shortest maturity on the left and progressively longer time periods on the right. The vertical or y-axis depicts the annualized yield to maturity.

Fixed income refers to any type of investment under which the borrower or issuer is obliged to make payments of a fixed amount on a fixed schedule. For example, the borrower may have to pay interest at a fixed rate once a year and repay the principal amount on maturity. Fixed-income securities can be contrasted with equity securities that create no obligation to pay dividends or any other form of income. Bonds carry a level of legal protections for investors that equity securities do not: in the event of a bankruptcy, bond holders would be repaid after liquidation of assets, whereas shareholders with stock often receive nothing.

Fixed-income arbitrage is a group of market-neutral-investment strategies that are designed to take advantage of differences in interest rates between varying fixed-income securities or contracts. Arbitrage in terms of investment strategy, involves buying securities on one market for immediate resale on another market in order to profit from a price discrepancy.

Fixed income analysis is the process of determining the value of a debt security based on an assessment of its risk profile, which can include interest rate risk, risk of the issuer failing to repay the debt, market supply and demand for the security, call provisions and macroeconomic considerations affecting its value in the future. It also addresses the likely price behavior in hedging portfolios. Based on such an analysis, a fixed income analyst tries to reach a conclusion as to whether to buy, sell, hold, hedge or avoid the particular security.

In finance, the yield spread or credit spread is the difference between the quoted rates of return on two different investments, usually of different credit qualities but similar maturities. It is often an indication of the risk premium for one investment product over another. The phrase is a compound of yield and spread.

The bond market is a financial market where participants can issue new debt, known as the primary market, or buy and sell debt securities, known as the secondary market. This is usually in the form of bonds, but it may include notes, bills, and so on for public and private expenditures. The bond market has largely been dominated by the United States, which accounts for about 39% of the market. As of 2021, the size of the bond market is estimated to be at $119 trillion worldwide and $46 trillion for the US market, according to the Securities Industry and Financial Markets Association (SIFMA).

Gilt-edged securities, also referred to as gilts, are bonds issued by the UK Government. The term is of British origin, and then referred to the debt securities issued by the Bank of England on behalf of His Majesty's Treasury, whose paper certificates had a gilt edge, hence the name.

A balloon payment mortgage is a mortgage that does not fully amortize over the term of the note, thus leaving a balance due at maturity. The final payment is called a balloon payment because of its large size. Balloon payment mortgages are more common in commercial real estate than in residential real estate today due to the prevalence of mortgages with longer periods of amortization, in particular, the 30-year fixed-rate mortgages. A balloon payment mortgage may have a fixed or a floating interest rate. The most common way of describing a balloon loan uses the terminology X due in Y, where X is the number of years over which the loan is amortized, and Y is the year in which the principal balance is due.

A bond fund or debt fund is a fund that invests in bonds, or other debt securities. Bond funds can be contrasted with stock funds and money funds. Bond funds typically pay periodic dividends that include interest payments on the fund's underlying securities plus periodic realized capital appreciation. Bond funds typically pay higher dividends than CDs and money market accounts. Most bond funds pay out dividends more frequently than individual bonds.

Reinvestment risk is a form of financial risk. It is primarily associated with fixed income securities, in the form of early redemption risk and coupon reinvestment risk.

In the United States, a mortgage note is a promissory note secured by a specified mortgage loan.

Dedicated portfolio theory, in finance, deals with the characteristics and features of a portfolio built to generate a predictable stream of future cash inflows. This is achieved by purchasing bonds and/or other fixed income securities that can and usually are held to maturity to generate this predictable stream from the coupon interest and/or the repayment of the face value of each bond when it matures. The goal is for the stream of cash inflows to exactly match the timing of a predictable stream of cash outflows due to future liabilities. For this reason it is sometimes called cash matching, or liability-driven investing. Determining the least expensive collection of bonds in the right quantities with the right maturities to match the cash flows is an analytical challenge that requires some degree of mathematical sophistication. College level textbooks typically cover the idea of “dedicated portfolios” or “dedicated bond portfolios” in their chapters devoted to the uses of fixed income securities.

References

- ↑ "Glossary of Investment Terms". Archived from the original on 2023-03-21. Retrieved 2023-12-02.

- ↑ "Maturity Date". web.archive.org. Retrieved 2023-12-02.

- ↑ "Glossary of Financial Terms". The Department of Financial Protection and Innovation. Archived from the original on 2021-10-19. Retrieved 2023-12-02.

| Authority control databases: National |

|---|

| | This finance-related article is a stub. You can help Wikipedia by expanding it. |