Microfinance is a of financial services targeting individuals and small businesses who lack access to conventional banking and related services. Microfinance includes microcredit, the provision of small loans to poor clients; savings and checking accounts; microinsurance; and payment systems, among other services. Microfinance services are designed to reach excluded customers, usually poorer population segments, possibly socially marginalized, or geographically more isolated, and to help them become self-sufficient. ID Ghana is an example of a microfinance institution.

Kotak Mahindra Bank Limited is an Indian banking and financial services company headquartered in Mumbai. It offers banking products and financial services for corporate and retail customers in the areas of personal finance, investment banking, life insurance, and wealth management. As of December 2023, the bank has 1,869 branches and 3,239 ATMs, including branches in GIFT City and DIFC (Dubai).

Mobile banking is a service provided by a bank or other financial institution that allows its customers to conduct financial transactions remotely using a mobile device such as a smartphone or tablet. Unlike the related internet banking it uses software, usually called an app, provided by the financial institution for the purpose. Mobile banking is usually available on a 24-hour basis. Some financial institutions have restrictions on which accounts may be accessed through mobile banking, as well as a limit on the amount that can be transacted. Mobile banking is dependent on the availability of an internet or data connection to the mobile device.

The term mobile commerce was originally coined in 1997 by Kevin Duffey at the launch of the Global Mobile Commerce Forum, to mean "the delivery of electronic commerce capabilities directly into the consumer’s hand, anywhere, via wireless technology." Many choose to think of Mobile Commerce as meaning "a retail outlet in your customer’s pocket."

Safaricom PLC is a listed Kenyan mobile network operator headquartered at Safaricom House in Nairobi, Kenya. It is the largest telecommunications provider in Kenya, and one of the most profitable companies in the East and Central Africa region. The company offers mobile telephony, mobile money transfer, consumer electronics, ecommerce, cloud computing, data, music streaming, and fibre optic services. It is most renowned as the home of M-PESA, a mobile banking SMS-based service.

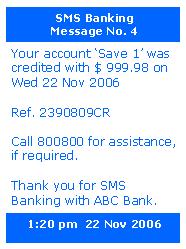

SMS banking' is a form of mobile banking. It is a facility used by some banks or other financial institutions to send messages to customers' mobile phones using SMS messaging, or a service provided by them which enables customers to perform some financial transactions using SMS.

Financial inclusion is the availability and equality of opportunities to access financial services. It refers to processes by which individuals and businesses can access appropriate, affordable, and timely financial products and services - which include banking, loan, equity, and insurance products. It provides paths to enhance inclusiveness in economic growth by enabling the unbanked population to access the means for savings, investment, and insurance towards improving household income and reducing income inequality

A banking agent is a retail or postal outlet contracted by a financial institution or a mobile network operator to process clients’ transactions. Rather than a branch teller, it is the owner or an employee of the retail outlet who conducts the transaction and lets clients deposit, withdraw, transfer funds, pay their bills, inquire about an account balance, or receive government benefits or a direct deposit from their employer. Banking agents can be pharmacies, supermarkets, convenience stores, lottery outlets, post offices, and more.

Citibank Berhad is a licensed commercial bank operating in Malaysia with its headquarters in Jalan Ampang, Kuala Lumpur. Citibank Berhad operates as a subsidiary of Citigroup Holding (Singapore) Private Limited, commencing its banking operations in Malaysia since 1959. Citibank Berhad was locally incorporated in 1994. Citibank Berhad has 11 branches spread across Kuala Lumpur, Selangor, Penang, Kuantan, Malacca and Johor, offering a wide range of banking and financial services including retail banking, institutional banking, and investment products and services.

Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 of India, engaged in the business of loans and advances, acquisition of shares, stock, bonds, hire-purchase insurance business or chit-fund business, but does not include any institution whose principal business is that of agriculture, industrial activity, purchase or sale of any goods or providing any services and sale/purchase/construction of immovable property.

M-PESA is a mobile phone-based money transfer service, payments and micro-financing service, launched in 2007 by Vodafone and Safaricom, the largest mobile network operator in Kenya. It has since expanded to Tanzania, Mozambique, DRC, Lesotho, Ghana, Egypt, Afghanistan, South Africa and Ethiopia. The rollouts in India, Romania, and Albania were terminated amid low market uptake. M-PESA allows users to deposit, withdraw, transfer money, pay for goods and services, access credit and savings, all with a mobile device.

Absa Bank Uganda Limited, formerly known as Barclays Bank of Uganda Limited, is a commercial bank in Uganda. It is licensed by the Bank of Uganda, the central bank and national banking regulator. The bank is a subsidiary of Absa Group Limited, a financial services conglomerate, based in South Africa, with banking subsidiaries in 12 African countries and representative offices in two other African countries. Absa Bank Group, whose shares trade on the JSE Limited, was reported to have total assets in excess of US$91 billion, as of October 2019.

Women's World Banking is a global nonprofit organization dedicated to women's economic empowerment through financial inclusion.

National Bank of Commerce (Tanzania), whose full name is National Bank of Commerce (Tanzania) Limited, sometimes referred to as NBC (Tanzania), or as NBC (Tanzania) Limited, is a commercial bank in Tanzania. It is one of the commercial banks licensed by the Bank of Tanzania, the country's central bank and the national banking regulator. In August 2019, the bank was fined TSh 1 billion (US$435,000) because of the failure to establish a data center in the East African nation.

Capitec Bank is a South African retail bank. As of February 2024 the bank was the largest retail bank in South Africa, based on number of customers, with 120,000 customers opening new accounts per month.

Hattha Bank (HKL) is a Cambodian bank and microfinance institution in Cambodia.

Bandhan Bank Ltd. is a banking and financial services company, headquartered in Kolkata.

Microfinance in Kenya consists of microfinance facilities and regulations in Kenya which has been developing since the mid 1990s. Legislation was passed in 2006 with the Micro Finance Act which became active in 2008. By 2010 there were more than twenty large micro finance institutions in Kenya, which provided US $1.5 billion to approximately 1.5 million active borrowers. With over 100,000 clients, Equity Bank Kenya had the largest share of business loans representing market share of 73.50% followed by Kenya Women Microfinance Bank with 12.06%. Most microfinance firms as in other countries have eligibility criteria which may include gender, age, a valid Kenyan ID, a business, an ability to repay the loan and be a customer of the institution.

Satin Creditcare Network Limited is a non-banking finance company (NBFC), licensed by the Reserve Bank of India. It was founded in 1990 by Mr. H P Singh. The company's offers financial requirements for excluded households at the bottom of the pyramid. Satin Creditcare Network Limited is a micro-finance institution (MFI) in the country with presence in 7 states and more than 12,00 villages.

Absa Bank Ghana Limited (ABGL), formerly known as Barclays Bank of Ghana Limited, is a commercial bank in Ghana, licensed by the Bank of Ghana, the country's central bank and national banking regulator. ABGL is a subsidiary of Absa Group Limited, a financial services conglomerate, headquartered in South Africa, with subsidiaries in 12 African countries and with assets in excess of US$87 billion as of 30 June 2017. Absa Group's shares trade on the Johannesburg Stock Exchange under the symbol ABG.