A student loan is a type of loan designed to help students pay for post-secondary education and the associated fees, such as tuition, books and supplies, and living expenses. It may differ from other types of loans in the fact that the interest rate may be substantially lower and the repayment schedule may be deferred while the student is still in school. It also differs in many countries in the strict laws regulating renegotiating and bankruptcy. This article highlights the differences of the student loan system in several major countries.

Tertiary student places in Australia are usually funded through the HECS-HELP scheme. This funding is in the form of loans that are not normal debts. They are repaid over time via a supplementary tax, using a sliding scale based on taxable income. As a consequence, loan repayments are only made when the former student has income to support the repayments. Discounts are available for early repayment. The scheme is available to citizens and permanent humanitarian visa holders. Means-tested scholarships for living expenses are also available. Special assistance is available to indigenous students.[1]

There has been criticism that the HECS-HELP scheme creates an incentive for people to leave the country after graduation, because those who do not file an Australian tax return do not make any repayments.[2]

The province of British Columbia allows the Insurance Corporation of British Columbia to withhold issuance or renewal of driver's license to those with delinquent student loan repayments or child support payments or unpaid court fines.[3] Students need to meet the qualification with an individual's direct educational costs and living expense to get the certificate to obtain a loan and this policy is directly controlled by the government.[4]

New Zealand provides student loans and allowances to tertiary students who satisfy the funding criteria. Full-time students can claim loans for both fees and living costs while part-time students can only claim training institution fees. While the borrower is a resident of New Zealand, no interest is charged on the loan. Loans are repaid when the borrower starts working and has income above the minimum threshold, once this occurs employers will deduct the student loan repayments from the salary at a fixed 12c in the dollar rate and these are collected by the New Zealand tax authority.

Thailand

The public sector is one of the most important sections in Thailand's higher education system. In addition, many public educational organizations usually receive profits from the students' tuition fees and the governments. Specifically, There are six various sections in the public sector's organization: colleges with the limited enrollment,universities which is opening to public, universities which is national autonomous, Rajabhat colleges, Ajamangala Universities of Technology, and polytechnic colleges.[5]

India

The Indian government has launched a portal, Vidya Lakshmi, for students seeking educational loans and five banks including SBI, IDBI Bank and Bank of India have integrated their system with the portal. Vidya Lakshmi was launched on the occasion of Independence Day i.e. 15 August 2015 for the benefit of students seeking educational loans.[6] Vidya Lakshmi was developed under three departments of India i.e. Department of Financial Services, Department of Higher Education and Indian Banks Association (IBA).[7] Vidya Lakshmi Portal has been developed under the Pradhan Mantri Vidya Lakshmi Karyakram and announced by the finance minister Shri Arun Jaitley in the budget speech of FY 2015–16. As of August 15, 2020, 37 banks were registered on the Vidya Lakshmi Portal and offered 137 loan schemes [8]

To bridge the constraint of increasing institutional fees, NSDL e-Governance in India launched the Vidyasaarathi portal to help students seeking scholarship for studies in India or overseas.[9][10]

The education loan is expected to grow at a rate of 32.3 percent in 2009-10, 39.8 percent each in 2010-11and 2011-12, and 44.8 percent during the period 2012–13 to 2014–15.

South Korea's student loans are managed by the Korea Student Aid Foundation (KOSAF) which was established in May 2009. According to the governmental philosophy that Korea's future depends on talent development and no student should quit studying due to financial reasons, they help students grow into talents that serve the nation and society as members of Korea.[11] Normally, in South Korea, the default rate of redemption is related to each student's academic personalities. For instance, comparing with other majors, students in fine arts and physics are supposed to possessing a higher default rate. Therefore, students in such majors would be inclined to a higher rate of unemployment and a higher risk of default in redemption. Also, people will tend to have an inferior quality of human capital if the period of unemployment is too long.[12]

Student loans in the United Kingdom are primarily provided by the state-owned Student Loans Company. Interest begins to accumulate on each loan payment as soon as the student receives it, but repayment is not required until the start of the next tax year after the student completes (or abandons) their education.[13]

Since 1998, repayments have been collected by HMRC via the tax system, and are calculated based on the borrower's current level of income. If the borrower's income is below a certain threshold (£15,000 per tax year for 2011/2012, £21,000 per tax year for 2012/2013), no repayments are required, though interest continues to accumulate.

Loans are canceled if the borrower dies or becomes permanently unable to work. Depending on when the loan was taken out and which part of the UK the borrower is from, they may also be canceled after a certain period of time usually after 30 years, or when the borrower reaches a certain age.

Student loans taken out between 1990 and 1998, in the introductory phase of the UK government's phasing in of student loans, were not subsequently collected through the tax system in the following years. The onus was (and still is) on the loan holder to prove their income falls below an annually calculated threshold set by the government if they wish to defer payment of their loan. A portfolio of early student loans from the 1990s was sold, by The Department for Business, Innovation and Skills in 2013. Erudio, a company financially backed by CarVal and Arrow Global was established to process applications for deferment and to manage accounts, following its successful purchasing bid of the loan portfolio in 2013.

There are complaints that graduates who have fully repaid their loans are still having £300 a month taken from their accounts and cannot get this stopped.[14]

In the United States, there are two types of student loans: federal loans sponsored by the federal government and private student loans, which broadly includes state-affiliated nonprofits and institutional loans provided by schools.[15] The overwhelming majority of student loans are federal loans. Federal loans can be "subsidized" or "unsubsidized." Interest does not accrue on subsidized loans while the students are in school. Student loans may be offered as part of a total financial aid package that may also include grants, scholarships, and/or work study opportunities. Whereas interest for most business investments is tax deductible, Student loan interest is generally not deductible. Critics contend that tax disadvantages to investments in education contribute to a shortage of educated labor, inefficiency, and slower economic growth.[who?][citation needed]

Prior to 2010, federal loans were also divided into direct loans (which are originated and funded by the federal government) and guaranteed loans, originated and held by private lenders but guaranteed by the government. The guaranteed lending program was eliminated in 2010 because of a widespread perception that the government guarantees boosted student lending companies' profits but did not benefit students by reducing student loan costs.[16]

Federal student loans are less expensive than private student loans. The federal government offers direct consolidation loans through the Federal Direct Loan Program. The new interest rate is the weighted average of the previous loans. Private loans don't qualify for this program.[citation needed] The interest rate of borrowers with federal student loans is nearly equal to the weighted average rate on the former loans while the new interest rate of private loans depends on the one-month London interbank offered rate. Therefore, these two student loans are different in both application and definition.[17] Losses on student loans are extremely low, even when students default, in part because these loans cannot be discharged in bankruptcy unless repaying the loan would create an "undue hardship" for the student borrower and dependents of the borrower.[18] In 2005, the bankruptcy laws were changed so that private educational loans also could not be readily discharged. Supporters of this change claimed that it would reduce student loan interest rates; critics said it would increase the lenders' profit.

Students can apply for loans to Stafford Loans with no risks; and there are around 1000 banks engaged in the student loan project.[citation needed] Students can also apply for student loans with the Department of Education which enables any school to take part in its Direct Loan project.[19]

Rising student debt

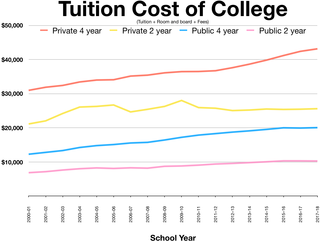

Federal aid policies expanded loan eligibility and shifted from grants to loans[20] starting the rising student debt. The Federal Pell Grant, a form of federal aid for higher education students that does not need to be re-paid, only provides a maximum annual grant of $6,195 per student for the 2019-2020 award year.[21] With the average annual tuition cost for a four year in-state public university averaging $26,590 for the 2019–2020 academic year,[22] many students are forced to take out student loans to bridge the gap between grants and their annual tuition costs. More students over the years have been actively enrolled in universities, with enrollment in for-profit universities growing by over 5 million in the past 10 years. For-profit universities enroll only 10% of the nations active college enrollment, yet hold nearly 20% of all federal student loan.[20] States have also deprived public support and shifted the financial burden onto students by increasing the cost of tuition.[23] With the median family income on a steady decline each year since 2007 up until 2012, it saw increasing difficulty for students to pay back college tuition out of savings and labor income.[24] Between 2002 and 2012, public spending on education dropped 30%, while total enrollment at public colleges and universities jumped 34%.[25] Ninety-two percent of student debt is loaned directly by the federal government.[26] In 2020, the amount of student loan debt had reached $1.6 trillion.[26]

Income-based repayment

The Income-based repayment (IBR) plan is an alternative to paying back federal student loans, which allows the borrowers to pay back loans based on how much they make, and not based how much money is actually owed.[27] Income-based repayment is a federal program and is not available for private loans.[28]

IBR plans generally cap loan payments at 10 percent of the student borrower's income. Deferred interest accrues, and the balance owed grows. However, after a certain number of years, the balance of the loan is forgiven. This period is 10 years if the student borrower works in the public sector (government or a nonprofit) and 25 years if the student works at a for-profit. Debt forgiveness may be treated as taxable income, but can be excluded as taxable under certain circumstances, like bankruptcy and insolvency.[29][30] Loans forgiven through the Public Service Loan Forgiveness program are not considered taxable income.[31]

Qualification

Most college students in the United States qualify for federal student loans.[32] Students can borrow the same amount of money, at the same price, regardless of their own income or their parents' incomes, regardless of their expected future income, and regardless of their credit history. Only students who have defaulted on federal student loans or have been convicted of drug offenses, and have not completed a rehabilitation program, are excluded. Borrowers from families with low income with separation are more likely to default than those from higher-income families. Also, borrowers entering repayment after their sophomore year are more likely to default.[33]

This is the image of the Percentage of Federal Student Loans in Default within age groups, Fiscal Year 2013. This chart shows that in 2013, around 17 percent of parent plus loans were in default from ages 65 to 74, and 30 percent of their own education loans were in default.

The amount students can borrow each year depends on their education level (undergraduate or graduate), and their status as dependent or independent. Undergraduates are eligible for subsidized loans, with no interest while the student is in school. Graduate students can borrow more per year.[16]

Private lenders use different underwriting criteria, including credit rating, income level, parents' income level, and other financial considerations. Students only borrow from private lenders when they exhaust the maximum borrowing limits under federal loans. Several scholars have advocated eliminating the borrowing limit on federal loans and enabling students to borrow according to their needs (tuition plus living expenses) and thereby eliminating high-cost private loans.[16]

Repayment

Federal student loan interest rates are established by Congress and listed in § 20 U.S.C. § 1087E(b). Because the interest rates are established by Congress, interest rates are a political decision. In 2010, the federal student loan program ran a multibillion-dollar "negative subsidy", or profit, for the federal government. Loans to graduate and professional students are especially profitable because of high-interest rates and low default rates.[34] Usually, the net flow of the default rate on student loans are strongly related to the nontraditional issuer and the flowing price of the tangible assets, unlike buildings or land.[clarification needed] However, in contrast to the positive correlation with the borrower, a change in the price normally leads to a negative influence on the default rate. These two aspects have been used to explain the Great Recession of student loan default, which had grown to nearly thirty percent.[35]

Some experts[specify] believe that the education of workers would bring societal benefits such as reducing stress on public services, reducing medical expenses, increasing incomes, and promoting employment rates. These people propose that federal student loan rates should be adjusted with specific courses, relative to the rate of risk and societal returns from various studies.[36][37]

Traditionally, repayment starts six months after graduation or leaving school.[citation needed]

It is important to note[according to whom?] that financial relief can provide a safety net for those under intense pressure to repay, leading many towards gaining income and avoiding defaulting.[38]

With federal student loans, the student may have multiple options for extending the repayment period. An extension of the loan term will reduce the monthly payment and increase the amount of total interest paid on the principal balance during the life of the loan (the unpaid interest and any penalties become capitalized, i.e. added to the loan balance). Extension options include extended payment periods offered by the original lender and federal loan consolidation. There are also other extension options including income-based repayment plans and hardship deferments.[citation needed]

The Master Promissory Note is an agreement between the lender and the borrower that promises to repay the loan. It is a binding legal contract.

In coverage through established media outlets, many borrowers have expressed feelings of victimization by the student loan corporations.[39][40][41] There is a comparison between these accounts and the college credit card trend in America during the 2000s, though the amounts owed by students on their student loans are almost always higher than the amount owed on credit cards.[42] Student loans cannot be discharged in a bankruptcy proceeding unless the debtor can demonstrate "undue hardship."[43] After the passage of the bankruptcy reform bill of 2005, even private student loans are not discharged during bankruptcy. This provided a credit risk free loan for the lender, averaging 7 percent a year.[44]

In 2007, Andrew Cuomo, then Attorney General of New York State, led an investigation into lending practices and anti-competitive relationships between student lenders and universities. Specifically, many universities steered student borrowers to "preferred lenders" which resulted in those borrowers incurring higher interest rates. Some of these "preferred lenders" allegedly rewarded university financial aid staff with "kickbacks".[citation needed] This has led to changes in lending policy at many major American universities. Many universities have also rebated millions of dollars in fees back to affected borrowers.[45][46]

In 2007, a false claims lawsuit was filed on behalf of the federal government by former Department of Education researcher Jon Oberg against Sallie Mae, Nelnet, and other lenders. Oberg argued that the lenders overcharged the U.S. government and defrauded taxpayers of millions and millions of dollars.[citation needed] In August 2010, Nelnet settled the lawsuit and paid $55 million.[47]

Since 2005, Bankruptcy reform lead debtors have to take the responsibility of private student loan debt in bankruptcy which can decline debtors’ intention of reducing costly defaults to declare bankruptcy.[48]

As of 2013, many economists are predicting a new economic crisis will emerge as a result of an estimated $1 trillion of student loan debt currently impacting two thirds of graduating college students in America.[49] However, most economists and investors believe that there is no student loan bubble.[50]

In his 2020 presidential campaign, Joe Biden promised student loan forgiveness.[51] 64% of Americans back student loan forgiveness of $10,000 for individuals earning up to $150,000 annually.[52]

Hong Kong

The loan scheme for Hong Kong students was introduced in 1969. This scheme aimed to help full-time students at two universities: the Chinese University of Hong Kong and Hong Kong University. The program was extended in 1976 to cover full-time students in the Hong Kong Polytechnic, and further extended in 1982 to cover post-advanced level students in the Hong Kong Baptist College. In 1984 loans were expanded to include students in the new city Polytechnic. The scheme is controlled by the secretary of the university and Polytechnic Grants Committee, which is advised by the Joint Committee On Student Finance. The applicant of the loan scheme must have resided or been domiciled in Hong Kong for three years immediately prior to application.[53] In 1990, a new government office, the Student Financial Assistance Agency, was also established to coordinate the administration of the student loan scheme.[54]

In finance, a loan is the transfer of money by one party to another with an agreement to pay it back. The recipient, or borrower, incurs a debt and is usually required to pay interest for the use of the money.

Debt consolidation is a form of debt refinancing that entails taking out one loan to pay off many others. This commonly refers to a personal finance process of individuals addressing high consumer debt, but occasionally it can also refer to a country's fiscal approach to consolidate corporate debt or government debt. The process can secure a lower overall interest rate to the entire debt load and provide the convenience of servicing only one loan or debt. Debt consolidation is sometimes offered by loan sharks, who charge clients exorbitant interest rates. Further regulation has been discussed as a result.

Student financial aid in the United States is funding that is available exclusively to students attending a post-secondary educational institution in the United States. This funding is used to assist in covering the many costs incurred in the pursuit of post-secondary education. Financial aid is available from federal and state governments, educational institutions, and private organizations. It can be awarded in the form of grants, loans, work-study, and scholarships. In order to apply for federal financial aid, students must first complete the Free Application for Federal Student Aid (FAFSA).

In finance, unsecured debt refers to any type of debt or general obligation that is not protected by a guarantor, or collateralized by a lien on specific assets of the borrower in the case of a bankruptcy or liquidation or failure to meet the terms for repayment. Unsecured debts are sometimes called signature debt or personal loans. These differ from secured debt such as a mortgage, which is backed by a piece of real estate.

College tuition in the United States is the cost of higher education collected by educational institutions in the United States, and paid by individuals. It does not include the tuition covered through general taxes or from other government funds, or that which is paid from university endowment funds or gifts. Tuition for college has increased as the value, quality, and quantity of education have increased. Many feel that increases in cost have not been accompanied by increases in quality, and that administrative costs are excessive. The value of a college education has become a topic of national debate in the U.S.

The Higher Education Act of 1965 (HEA) was legislation signed into United States law on November 8, 1965, as part of President Lyndon Johnson's Great Society domestic agenda. Johnson chose Texas State University, his alma mater, as the signing site. The law was intended "to strengthen the educational resources of our colleges and universities and to provide financial assistance for students in postsecondary and higher education". It increased federal money given to universities, created scholarships, gave low-interest loans for students, and established a National Teachers Corps. The "financial assistance for students" is covered in Title IV of the HEA.

A Stafford Loan was a student loan offered from the United States Department of Education to eligible students enrolled in accredited American institutions of higher education to help finance their education. The terms of the loans are described in Title IV of the Higher Education Act of 1965, which guarantees repayment to the lender if a student defaults. As of July 1, 2010, Stafford Loans are no longer being offered, having been replaced with the William D. Ford Federal Direct Student Loan Program.

The Federal Family Education Loan (FFEL) Program was a system of private student loans which were subsidized and guaranteed by the United States federal government. The program issued loans from 1965 until it was ended in 2010. Similar loans are now provided under the Federal Direct Student Loan Program, which are federal loans issued directly by the United States Department of Education.

The William D. Ford Federal Direct Loan Program provides "low-interest loans for students and parents to help pay for the cost of a student's education after high school. The lender is the U.S. Department of Education ... rather than a bank or other financial institution." It is the largest single source of federal financial aid for students and their parents pursuing post-secondary education and for many it is the first financial obligation they incur, leaving them with debt to be paid over a period of time that can be a decade or more as the average student takes 19.4 years. The program is named after William D. Ford, a former member of the U.S. House of Representatives from Michigan.

A private student loan is a financing option for higher education in the United States that can supplement, but should not replace, federal loans, such as Stafford loans, Perkins loans and PLUS loans. Private loans, which are heavily advertised, do not have the forbearance and deferral options available with federal loans. In contrast with federal subsidized loans, interest accrues while the student is in college, even if repayment does not begin until after graduation. While unsubsidized federal loans do have interest charges while the student is studying, private student loan rates are usually higher, sometimes much higher. Fees vary greatly, and legal cases have reported collection charges reaching 50% of amount of the loan. Since 2011, most private student loans are offered with zero fees, effectively rolling the fees into the interest rates.

Federal Student Aid (FSA), an office of the U.S. Department of Education, is the largest provider of student financial aid in the United States. Federal Student Aid provides student financial assistance in the form of grants, loans, and work-study funds. FSA is a Performance-Based Organization, and was the first PBO to be established in the US government.

In the United States, the Federal Direct Student Loan Program (FDLP) includes consolidation loans that allow students to consolidate Stafford Loans, Graduate PLUS Loans, and Federal Perkins Loans into one single debt.

A mortgage loan or simply mortgage, in civil law jurisdictions known also as a hypothec loan, is a loan used either by purchasers of real property to raise funds to buy real estate, or by existing property owners to raise funds for any purpose while putting a lien on the property being mortgaged. The loan is "secured" on the borrower's property through a process known as mortgage origination. This means that a legal mechanism is put into place which allows the lender to take possession and sell the secured property to pay off the loan in the event the borrower defaults on the loan or otherwise fails to abide by its terms. The word mortgage is derived from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure. A mortgage can also be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

In finance, subprime lending is the provision of loans to people in the United States who may have difficulty maintaining the repayment schedule. Historically, subprime borrowers were defined as having FICO scores below 600, although this threshold has varied over time.

Student loans and grants in the United Kingdom are primarily provided by the government through the Student Loans Company (SLC), an executive non-departmental public body. The SLC is responsible for Student Finance England and Student Finance Wales, and is a delivery partner of Student Finance NI and the Student Awards Agency for Scotland. Most undergraduate university students resident in the United Kingdom are eligible for student loans, and some students on teacher training courses may also apply for loans. Student loans also became available from the 2016/17 academic year to postgraduate students who study a taught Masters, research or Doctoral course.

In the United States, student loans are a form of financial aid intended to help students access higher education. In 2018, 70 percent of higher education graduates had used loans to cover some or all of their expenses. With notable exceptions, student loans must be repaid, in contrast to other forms of financial aid such as scholarships, which are not repaid, and grants, which rarely have to be repaid. Student loans may be discharged through bankruptcy, but this is difficult. Research shows that access to student loans increases credit-constrained students' degree completion, later-life earnings, and student loan repayment while having no impact on overall debt.

Student debt refers to the debt incurred by an individual to pay for education-related expenses. This debt is most commonly assumed to pay for tertiary education, such as university.

Student loans in South Korea, are student loans provided to South Korea's students that are managed by the Korea Student Aid Foundation (KOSAF) which was established in May 2009. According to the governmental philosophy that Korea's future depends on talent development and no student should quit studying due to financial reasons, they help students grow into talents that serve the nation and society as members of Korea. Through the management of Korea's national scholarship programs, student loan programs, and talent development programs, KOSAF offers customized student aid services and student loan program is one of their major tasks.

A repayment plan is a structured repaying of funds that have been loaned to an individual, business or government over either a standard or extended period of time, typically alongside a payment of interest. Repayment plans are prominent within the financial industry of a national economy where liquid funds are in high demand to assist in investment opportunities, governmental expenditure or personal finance. The term first saw prominence with its use by the International Monetary Fund to describe its form of financial loan repayment from individual nations. Typically, the term "repayment plan" refers to the system of Federal Student Aid in the United States of America, which assists in covering tertiary education expenses of domestic students.

Financial issues facing students in the United States include the rising cost of tuition, as well as ancillaries, such as room and board, textbook and coursework costs, personal expenses, and transportation.

↑ Free Uni for Artful Dodgers Incentives for Australians to leave the country after graduation (Retrieved 2014-08-22)

↑ Kines, Lindsay (March 12, 2015). "Pay debts or put your driver's licence at risk; ICBC asked to collect on student loans, court fines". Times - Colonist. Victoria, British Columbia. p.S5.

↑ Finnie, Ross (November 2001). "Measuring the load, easing the burden: Canada's student loan programs and the revitalization of Canadian postsecondary education". Commentary – C.D. Howe Institute (154–156). ISSN0824-8001. ProQuest216599241.

↑ Somkiat, Tangkitvanich; Manasboonphempool, Areeya (2010). "Evaluating the Student Loan Fund of Thailand". Economics of Education Review. 29 (5): 710–721. doi:10.1016/j.econedurev.2010.04.007.

1 2 3 Jonathan Glater, The Other Big Test: Why Congress Should Allow College Students to Borrow More Through Federal Aid Programs, 14 N.Y.U. J. LEGIS. & PUB. POL’Y 11, 37 (2011)

↑ Andriotis Anna, Maria (Jun 2014). "WEEKEND INVESTOR --- College Debt: Easing the Burden --- Despite moves to expand a major student-loan relief program, many borrowers still won't qualify; Here are the best options for graduates with federal or private student loans". The Wall Street Journal. ProQuest1535344338.

↑ John A. E. Pottow, The Nondischargeability of Student Loans in Personal Bankruptcy Proceedings: The Search for a Theory, 44 CAN. BUS. L.J. 245, 249-250 (2006)

↑ Petri, Thomas E. (Feb 2008). "No Worry About Getting Student Loans'". New York Dow Jones & Company Inc. ProQuest399057075.

↑ Philip G. Schrag & Charles W. Pruett, Coordinating Loan Repayment Assistance Programs with New Federal Legislation, 60 J. LEGAL EDUC. 583, 590-597 (2010)

↑ "Public Service Loan Forgiveness FAQ". Studentaid.ed.gov. Retrieved 2022-04-20. According to the Internal Revenue Service (IRS), student loan amounts forgiven under PSLF aren't considered income for tax purposes.

↑ DEBORAH KALCEVIC & JUSTIN HUMPHREY, CONGRESSIONAL BUDGET OFFICE, CBO MARCH 2012 BASELINE PROJECTIONS FOR THE STUDENT LOAN AND PELL GRANT PROGRAMS, Tables 2, 3

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.