A personal budget (for an individual) or household budget (for a group sharing a household) [1] is a plan for the coordination of income and expenses. [2]

A personal budget (for an individual) or household budget (for a group sharing a household) [1] is a plan for the coordination of income and expenses. [2]

Personal budgets are usually created to help an individual or a household of people to control their spending and achieve their financial goals. Having a budget can help people feel more in control of their finances and make it easier for them to not overspend and to save money. [3] People who budget their money are less likely to amass large debts, are more likely to lead comfortable lives in retirement, and are better prepared for emergencies.

In the most basic form of creating a personal budget the person needs to calculate their net income, track their spending over a set period of time, set goals based on the information previously gathered, make a plan to achieve these goals, and adjust their spending based on the plan. [3] There exist many methods of budgeting to help people do this.

The 50/30/20 budget is a simple plan that sorts personal expenses into three categories: "needs" (basic necessities), "wants", and savings. 50% of one's net income then goes towards needs, 30% towards wants, and 20% towards savings. [4]

In the pay yourself first budget people first save at least 20% of their net income, and then freely spend the remaining 80%. They can also choose a 70/30, 60/40, or 50/50 budget for more savings. The most important part of this method is to put one's savings apart before spending on anything else. [5]

This method is a variation of the pay yourself first budget, in which people create multiple savings accounts, each for one specific goal (such as a vacation or a new car), and each with an amount of money that should be reached by a specific date. They then divide the amount of money needed by the timeline to calculate how much they should save each month.[ citation needed ]

For this method, people need to use cash instead of debit or credit cards. They need to allocate their net income into categories (e.g. groceries), withdraw the cash allocated for each category, and put them into envelopes. Any time they want to buy something in one of the categories, they only take the designated envelope so that they cannot overspend.

In zero-based budgeting, all of one's net income must be allocated ahead of spending. Zero-based budgeting involves dividing income into different expense categories, ensuring that all funds have been assigned a purpose, and at the end of the month there is a zero balance in the budget.[ citation needed ]

Several personal finance softwares and mobile apps have been developed to help people with managing their money. Some of them can be used for budgeting and expense tracking, others mainly for one's investment portfolio. There are both free and paid options.

Disposable income is total personal income minus current taxes on income. In national accounts definitions, personal income minus personal current taxes equals disposable personal income. Subtracting personal outlays yields personal savings, hence the income left after paying away all the taxes is referred to as disposable income.

An expense is an item requiring an outflow of money, or any form of fortune in general, to another person or group as payment for an item, service, or other category of costs. For a tenant, rent is an expense. For students or parents, tuition is an expense. Buying food, clothing, furniture, or an automobile is often referred to as an expense. An expense is a cost that is "paid" or "remitted", usually in exchange for something of value. Something that seems to cost a great deal is "expensive". Something that seems to cost little is "inexpensive". "Expenses of the table" are expenses for dining, refreshments, a feast, etc.

The government budget balance, also referred to as the general government balance, public budget balance, or public fiscal balance, is the difference between government revenues and spending. For a government that uses accrual accounting the budget balance is calculated using only spending on current operations, with expenditure on new capital assets excluded. A positive balance is called a government budget surplus, and a negative balance is a government budget deficit. A government budget presents the government's proposed revenues and spending for a financial year.

Personal finance is the financial management that an individual or a family unit performs to budget, save, and spend monetary resources in a controlled manner, taking into account various financial risks and future life events.

A budget is a calculation plan, usually but not always financial, for a defined period, often one year or a month. A budget may include anticipated sales volumes and revenues, resource quantities including time, costs and expenses, environmental impacts such as greenhouse gas emissions, other impacts, assets, liabilities and cash flows. Companies, governments, families, and other organizations use budgets to express strategic plans of activities in measurable terms.

A tax cut represents a decrease in the amount of money taken from taxpayers to go towards government revenue. Tax cuts decrease the revenue of the government and increase the disposable income of taxpayers. Tax cuts usually refer to reductions in the percentage of tax paid on income, goods and services. As they leave consumers with more disposable income, tax cuts are an example of an expansionary fiscal policy. Tax cuts also include reduction in tax in other ways, such as tax credit, deductions and loopholes.

In general usage, a financial plan is a comprehensive evaluation of an individual's current pay and future financial state by using current known variables to predict future income, asset values and withdrawal plans. This often includes a budget which organizes an individual's finances and sometimes includes a series of steps or specific goals for spending and saving in the future. This plan allocates future income to various types of expenses, such as rent or utilities, and also reserves some income for short-term and long-term savings. A financial plan is sometimes referred to as an investment plan, but in personal finance, a financial plan can focus on other specific areas such as risk management, estates, college, or retirement.

A child trust fund (CTF) is a long-term savings or investment account for children in the United Kingdom. New accounts can no longer be created as of 2011, but existing accounts can receive new money: the accounts were replaced by Junior ISAs.

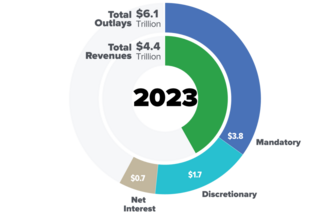

The United States budget comprises the spending and revenues of the U.S. federal government. The budget is the financial representation of the priorities of the government, reflecting historical debates and competing economic philosophies. The government primarily spends on healthcare, retirement, and defense programs. The non-partisan Congressional Budget Office provides extensive analysis of the budget and its economic effects. CBO estimated in February 2024 that Federal debt held by the public is projected to rise from 99 percent of GDP in 2024 to 116 percent in 2034 and would continue to grow if current laws generally remained unchanged. Over that period, the growth of interest costs and mandatory spending outpaces the growth of revenues and the economy, driving up debt. Those factors persist beyond 2034, pushing federal debt higher still, to 172 percent of GDP in 2054.

Dissaving is negative saving. If spending is greater than disposable income, dissaving is taking place. This spending is financed by already accumulated savings, such as money in a savings account, or it can be borrowed. Household dissaving therefore corresponds to an absolute decrease in their financial investments.

A government budget is a projection of the government's revenues and expenditure for a particular period, often referred to as a financial or fiscal year, which may or may not correspond with the calendar year. Government revenues mostly include taxes while expenditures consist of government spending. A government budget is prepared by the Central government or other political entity. In most parliamentary systems, the budget is presented to the legislature and often requires approval of the legislature. The government implements economic policy through this budget and realizes its program priorities. Once the budget is approved, the use of funds from individual chapters is in the hands of government ministries and other institutions. Revenues of the state budget consist mainly of taxes, customs duties, fees, and other revenues. State budget expenditures cover the activities of the state, which are either given by law or the constitution. The budget in itself does not appropriate funds for government programs, hence the need for additional legislative measures. The word budget comes from the Old French brunette.

Zero-based budgeting (ZBB) is a budgeting method that requires all expenses to be justified and approved in each new budget period, typically each year. It was developed by Peter Pyhrr in the 1970s. This budgeting method analyzes an organization's needs and costs by starting from a "zero base" at the beginning of every period. The intended outcome is to access the efficient use of resources by determining if services can be provided at a lower cost. However, the saving comes at the expense of a complete restructuring every budget cycle. Although used at least partially in both government and the private sector, there is some doubt whether ZBB has ever been utilized to its fullest extent in any organization.

The Balanced Budget Act of 1997 was an omnibus legislative package enacted by the United States Congress, using the budget reconciliation process, and designed to balance the federal budget by 2002. This act was enacted during Bill Clinton's second term as president.

The Wealthy Barber is a financial planning book franchise by Canadian author David Chilton. The first book in the series was in the business fable genre, using the story of fictional characters to convey financial advice.

Retirement planning, in a financial context, refers to the allocation of savings or revenue for retirement. The goal of retirement planning is to achieve financial independence.

You Need a Budget (YNAB) (pronounced ) is an online personal budgeting program based on the envelope system developed by a privately owned American company of the same name. It is available via any internet browser or a mobile app.

The envelope system, also known as the envelope budgeting method or cash stuffing, is a popular personal budgeting method for visualizing and maintaining a flexible budget. The key idea is to prioritize cash income to meet separate categories of household expenses in physically separate envelopes.

At retirement, individuals stop working and no longer get employment earnings, and enter a phase of their lives, where they rely on the assets they have accumulated, to supply money for their spending needs for the rest of their lives. Retirement spend-down, or withdrawal rate, is the strategy a retiree follows to spend, decumulate or withdraw assets during retirement.

The Moonlight Clan is a large group of people who expend their entire salary before the end of each month. The term is derived from a lunar cycle. While yue guang translates directly to "moonlight", it is also a pun derived from the combination of its individual words, yue and guang. Zu refers to a group of people who shares this characteristic. In the United States, a comparable notion is referred to as "living paycheck to paycheck". "Moonlight clan" is a relatively new Chinese neologism to describe young workers who spend their salaries faster than they earn it. The Moonlite are generally younger generations. They are different from their parents' diligent and thrifty consumption concepts. To chase new trends and have fun, they don't care about the cost as long as they like. Material life is what they yearn for, but also the motivation to earn money. The older generation believes that "saving is more significant than spending", and they are very upset about their behavior; however, their motto is "spending can lead to make more money". The Moonlite are companies' favorite group of consumers, since they have strong purchasing power from desires; more importantly, they have the ability to make money and have money to spend.

The FIREmovement is a lifestyle/investment plan with the goal of gaining financial independence and retiring early through savings. The model became particularly popular among millennials in the 2010s, gaining traction through online communities via information shared in blogs, podcasts, and online discussion forums.