The United States has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP.

The Canada Revenue Agency is the revenue service of the Canadian federal government, and most provincial and territorial governments. The CRA collects taxes, administers tax law and policy, and delivers benefit programs and tax credits. Legislation administered by the CRA includes the Income Tax Act, parts of the Excise Tax Act, and parts of laws relating to the Canada Pension Plan, employment insurance (EI), tariffs and duties. The agency also oversees the registration of charities in Canada, and enforces much of the country's tax laws.

A tax refund or tax rebate is a payment to the taxpayer due to the taxpayer having paid more tax than they owed.

A child tax credit (CTC) is a tax credit for parents with dependent children given by various countries. The credit is often linked to the number of dependent children a taxpayer has and sometimes the taxpayer's income level. For example, with the Child Tax Credit in the United States, only families making less than $400,000 per year may claim the full CTC. Similarly, in the United Kingdom, the tax credit is only available for families making less than £42,000 per year.

Tax withholding, also known as tax retention, pay-as-you-earn tax or tax deduction at source, is income tax paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, tax withholding applies to employment income. Many jurisdictions also require withholding taxes on payments of interest or dividends. In most jurisdictions, there are additional tax withholding obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use tax withholding as a means to combat tax evasion, and sometimes impose additional tax withholding requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

The Offer in Compromise (OIC) program, in the United States, is an Internal Revenue Service (IRS) program under 26 U.S.C. § 7122, which allows qualified individuals with an unpaid tax debt to negotiate a settled amount that is less than the total owed to clear the debt. A taxpayer uses the checklist in the Form 656, OIC package to determine if the taxpayer is eligible for the program. The objective of the OIC program is to accept a compromise when acceptance is in the best interests of both the taxpayer and the government, and promotes voluntary compliance with all future payment and filing requirements.

The United States federal government and most state governments impose an income tax. They are determined by applying a tax rate, which may increase as income increases, to taxable income, which is the total income less allowable deductions. Income is broadly defined. Individuals and corporations are directly taxable, and estates and trusts may be taxable on undistributed income. Partnerships are not taxed, but their partners are taxed on their shares of partnership income. Residents and citizens are taxed on worldwide income, while nonresidents are taxed only on income within the jurisdiction. Several types of credits reduce tax, and some types of credits may exceed tax before credits. Most business expenses are deductible. Individuals may deduct certain personal expenses, including home mortgage interest, state taxes, contributions to charity, and some other items. Some deductions are subject to limits, and an Alternative Minimum Tax (AMT) applies at the federal and some state levels.

Income taxes in Canada constitute the majority of the annual revenues of the Government of Canada, and of the governments of the Provinces of Canada. In the fiscal year ending March 31, 2018, the federal government collected just over three times more revenue from personal income taxes than it did from corporate income taxes.

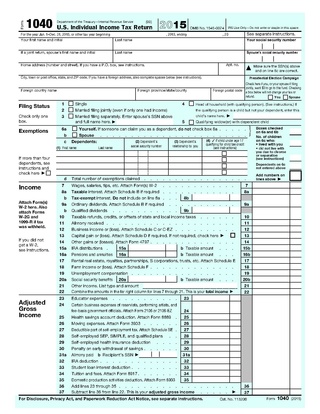

The United States Internal Revenue Service (IRS) uses forms for taxpayers and tax-exempt organizations to report financial information, such as to report income, calculate taxes to be paid to the federal government, and disclose other information as required by the Internal Revenue Code (IRC). There are over 800 various forms and schedules. Other tax forms in the United States are filed with state and local governments.

The Household and Dependent Care Credit is a nonrefundable tax credit available to United States taxpayers. Taxpayers that care for a qualifying individual are eligible. The purpose of the credit is to allow the taxpayer to be gainfully employed. This credit is created by 26 U.S. Code (U.S.C) § 21, section 21 of the Internal Revenue Code (IRC).

An adoption tax credit is a tax credit offered to adoptive parents to encourage adoption in the United States. Section 36C of the United States Internal Revenue code offers a credit for “qualified adoption expenses” paid or incurred by individual taxpayers.

The Nonbusiness energy property tax credit, in the United States, provides a nonrefundable personal tax credit for Federal income tax purposes, for making a home more energy efficient. This credit was added to the Internal Revenue Code by the Energy Policy Act of 2005. The nonbusiness energy property credit expired on December 31, 2017, but was retroactively extended for tax years 2018 and 2019 on December 20, 2019 as part of the Further Consolidated Appropriations Act, 2020. Further information about the legislation that extended the credit is at IRS.gov/Extenders.

The Economic Stimulus Act of 2008 was an Act of Congress providing for several kinds of economic stimuli intended to boost the United States economy in 2008 and to avert a recession, or ameliorate economic conditions. The stimulus package was passed by the U.S. House of Representatives on January 29, 2008, and in a slightly different version by the U.S. Senate on February 7, 2008. The Senate version was then approved in the House the same day. It was signed into law on February 13, 2008, by President George W. Bush with the support of both Democratic and Republican lawmakers. The law provides for tax rebates to low- and middle-income U.S. taxpayers, tax incentives to stimulate business investment, and an increase in the limits imposed on mortgages eligible for purchase by government-sponsored enterprises. The total cost of this bill was projected at $152 billion for 2008.

The United States federal earned income tax credit or earned income credit is a refundable tax credit for low- to moderate-income working individuals and couples, particularly those with children. The amount of EITC benefit depends on a recipient's income and number of children. Low-income adults with no children are eligible. For a person or couple to claim one or more persons as their qualifying child, requirements such as relationship, age, and shared residency must be met.

The American Opportunity Tax Credit is a partially refundable tax credit first detailed in Section 1004 of the American Recovery and Reinvestment Act of 2009.

The Lifetime Learning Credit, provided by 26 U.S.C. § 25A(b), is available to taxpayers in the United States who have incurred education expenses. For this credit to be claimed by a taxpayer, the student must attend school on at least a part-time basis. The credit can be claimed for education expenses incurred by the taxpayer, the taxpayer's spouse, or the taxpayer's dependent.

The alternative minimum tax (AMT) is a tax imposed by the United States federal government in addition to the regular income tax for certain individuals, estates, and trusts. As of tax year 2018, the AMT raises about $5.2 billion, or 0.4% of all federal income tax revenue, affecting 0.1% of taxpayers, mostly in the upper income ranges.

A tax return is the completion of documentation that calculates an entity or individual's income earned and the amount of taxes to be paid to the government or government organizations or, potentially, back to the taxpayer.

A flow-through share (FTS) is a tax-based financing incentive that is available to, among others, the mining sector. A FTS is a type of share issued by a corporation to a taxpayer, pursuant to an agreement with the corporation under which the issuing corporation agrees to incur eligible exploration expenses in an amount up to the consideration paid by the taxpayer for the shares.

The United States federal child tax credit (CTC) is a partially-refundable tax credit for parents with dependent children. It provides $2,000 in tax relief per qualifying child, with up to $1,400 of that refundable (subject to a refundability threshold, phase-in and phase-out). In 2021, following the passage of the American Rescue Plan Act of 2021, it was temporarily raised to $3,600 per child under the age of 6 and $3,000 per child between the ages of 6 and 17; it was also made fully-refundable and half was paid out as monthly benefits. This reverted back to the previous in 2022. The CTC is scheduled to revert to a $1,000 credit after 2025.