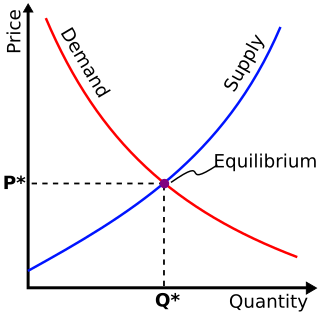

In economics, specifically general equilibrium theory, a perfect market, also known as an atomistic market, is defined by several idealizing conditions, collectively called perfect competition, or atomistic competition. In theoretical models where conditions of perfect competition hold, it has been demonstrated that a market will reach an equilibrium in which the quantity supplied for every product or service, including labor, equals the quantity demanded at the current price. This equilibrium would be a Pareto optimum.

Comparative advantage in an economic model is the advantage over others in producing a particular good. A good can be produced at a lower relative opportunity cost or autarky price, i.e. at a lower relative marginal cost prior to trade. Comparative advantage describes the economic reality of the gains from trade for individuals, firms, or nations, which arise from differences in their factor endowments or technological progress.

This aims to be a complete article list of economics topics:

Cost is the value of money that has been used up to produce something or deliver a service, and hence is not available for use anymore. In business, the cost may be one of acquisition, in which case the amount of money expended to acquire it is counted as cost. In this case, money is the input that is gone in order to acquire the thing. This acquisition cost may be the sum of the cost of production as incurred by the original producer, and further costs of transaction as incurred by the acquirer over and above the price paid to the producer. Usually, the price also includes a mark-up for profit over the cost of production.

Environmental full-cost accounting (EFCA) is a method of cost accounting that traces direct costs and allocates indirect costs by collecting and presenting information about the possible environmental costs and benefits or advantages – in short, about the "triple bottom line" – for each proposed alternative. It is one aspect of true cost accounting (TCA), along with Human capital and Social capital. As definitions for "true" and "full" are inherently subjective, experts consider both terms problematic.

In business, a competitive advantage is an attribute that allows an organization to outperform its competitors.

An expense is an item requiring an outflow of money, or any form of fortune in general, to another person or group as payment for an item, service, or other category of costs. For a tenant, rent is an expense. For students or parents, tuition is an expense. Buying food, clothing, furniture, or an automobile is often referred to as an expense. An expense is a cost that is "paid" or "remitted", usually in exchange for something of value. Something that seems to cost a great deal is "expensive". Something that seems to cost little is "inexpensive". "Expenses of the table" are expenses for dining, refreshments, a feast, etc.

Managerial economics is a branch of economics involving the application of economic methods in the organizational decision-making process. Economics is the study of the production, distribution, and consumption of goods and services. Managerial economics involves the use of economic theories and principles to make decisions regarding the allocation of scarce resources. It guides managers in making decisions relating to the company's customers, competitors, suppliers, and internal operations.

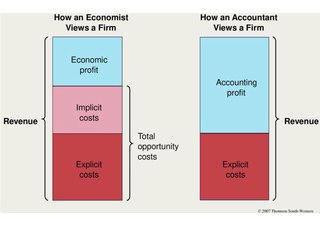

Economic cost is the combination of losses of any goods that have a value attached to them by any one individual. Economic cost is used mainly by economists as means to compare the prudence of one course of action with that of another. The comparison includes the gains and losses precluded by taking a course of action as well as those of the course taken itself. Economic cost differs from accounting cost because it includes opportunity cost.

In economics, an implicit cost, also called an imputed cost, implied cost, or notional cost, is the opportunity cost equal to what a firm must give up in order to use a factor of production for which it already owns and thus does not pay rent. It is the opposite of an explicit cost, which is borne directly. In other words, an implicit cost is any cost that results from using an asset instead of renting it out, selling it, or using it differently. The term also applies to foregone income from choosing not to work.

Operating surplus is an accounting concept used in national accounts statistics and in corporate and government accounts. It is the balancing item of the Generation of Income Account in the UNSNA. It may be used in macro-economics as a proxy for total pre-tax profit income, although entrepreneurial income may provide a better measure of business profits. According to the 2008 SNA, it is the measure of the surplus accruing from production before deducting property income, e.g., land rent and interest.

In the field of accounting, when reporting the financial statements of a company, accounting constraints are boundaries, limitations, or guidelines.

Advanced Placement (AP) Macroeconomics is an Advanced Placement macroeconomics course for high school students that culminates in an exam offered by the College Board.

Engineering economics, previously known as engineering economy, is a subset of economics concerned with the use and "...application of economic principles" in the analysis of engineering decisions. As a discipline, it is focused on the branch of economics known as microeconomics in that it studies the behavior of individuals and firms in making decisions regarding the allocation of limited resources. Thus, it focuses on the decision making process, its context and environment. It is pragmatic by nature, integrating economic theory with engineering practice. But, it is also a simplified application of microeconomic theory in that it assumes elements such as price determination, competition and demand/supply to be fixed inputs from other sources. As a discipline though, it is closely related to others such as statistics, mathematics and cost accounting. It draws upon the logical framework of economics but adds to that the analytical power of mathematics and statistics.

In economics, profit is the difference between revenue that an economic entity has received from its outputs and total costs of its inputs, also known as surplus value. It is equal to total revenue minus total cost, including both explicit and implicit costs.

A firm will choose to implement a shutdown of production when the revenue received from the sale of the goods or services produced cannot even cover the variable costs of production. In that situation, the firm will experience a higher loss when it produces, compared to not producing at all.

The following outline is provided as an overview of and topical guide to economics:

Return on investment (ROI) or return on costs (ROC) is the ratio between net income and investment. A high ROI means the investment's gains compare favourably to its cost. As a performance measure, ROI is used to evaluate the efficiency of an investment or to compare the efficiencies of several different investments. In economic terms, it is one way of relating profits to capital invested.

In any technical subject, words commonly used in everyday life acquire very specific technical meanings, and confusion can arise when someone is uncertain of the intended meaning of a word. This article explains the differences in meaning between some technical terms used in economics and the corresponding terms in everyday usage.

This glossary of economics is a list of definitions containing terms and concepts used in economics, its sub-disciplines, and related fields.