International Financial Reporting Standards, commonly called IFRS, are accounting standards issued by the IFRS Foundation and the International Accounting Standards Board (IASB). They constitute a standardised way of describing the company’s financial performance and position so that company financial statements are understandable and comparable across international boundaries. They are particularly relevant for companies with shares or securities listed on a public stock exchange.

In accounting, an economic item's historical cost is the original nominal monetary value of that item. Historical cost accounting involves reporting assets and liabilities at their historical costs, which are not updated for changes in the items' values. Consequently, the amounts reported for these balance sheet items often differ from their current economic or market values.

Financial instruments are monetary contracts between parties. They can be created, traded, modified and settled. They can be cash (currency), evidence of an ownership interest in an entity or a contractual right to receive or deliver in the form of currency (forex); debt ; equity (shares); or derivatives.

The Financial Accounting Standards Board (FASB) is a private, non-profit organization standard-setting body whose primary purpose is to establish and improve Generally Accepted Accounting Principles (GAAP) within the United States in the public's interest. The Securities and Exchange Commission (SEC) designated the FASB as the organization responsible for setting accounting standards for public companies in the US. The FASB replaced the American Institute of Certified Public Accountants' (AICPA) Accounting Principles Board (APB) on July 1, 1973.

Mark-to-market or fair value accounting refers to accounting for the "fair value" of an asset or liability based on the current market price, or the price for similar assets and liabilities, or based on another objectively assessed "fair" value. Fair value accounting has been a part of Generally Accepted Accounting Principles (GAAP) in the United States since the early 1990s, and is now regarded as the "gold standard" in some circles. Failure to use it is viewed as the cause of the Orange County Bankruptcy, even though its use is considered to be one of the reasons for the Enron scandal and the eventual bankruptcy of the company, as well as the closure of the accounting firm Arthur Andersen.

In accounting and in most schools of economic thought, fair value is a rational and unbiased estimate of the potential market price of a good, service, or asset. The derivation takes into account such objective factors as the costs associated with production or replacement, market conditions and matters of supply and demand. Subjective factors may also be considered such as the risk characteristics, the cost of and return on capital, and individually perceived utility.

Consolidated financial statements are the "financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flows of the parent company and its subsidiaries are presented as those of a single economic entity", according to International Accounting Standard 27 "Consolidated and separate financial statements", and International Financial Reporting Standard 10 "Consolidated financial statements".

Note: Reference cited below, FAS130, remains the most current accounting literature in the United States on this topic.

Hedge accounting is an accountancy practice, the aim of which is to provide an offset to the mark-to-market movement of the derivative in the profit and loss account. There are two types of hedge recognized. For a fair value hedge, the offset is achieved either by marking-to-market an asset or a liability which offsets the P&L movement of the derivative. For a cash flow hedge, some of the derivative volatility is placed into a separate component of the entity's equity called the cash flow hedge reserve. Where a hedge relationship is effective, most of the mark-to-market derivative volatility will be offset in the profit and loss account. Hedge accounting entails much compliance - involving documenting the hedge relationship and both prospectively and retrospectively proving that the hedge relationship is effective.

Launched prior to the millennium, FAS 133 Accounting for Derivative Instruments and Hedging Activities provided an "integrated accounting framework for derivative instruments and hedging activities."

Inflation accounting comprises a range of accounting models designed to correct problems arising from historical cost accounting in the presence of high inflation and hyperinflation. For example, in countries experiencing hyperinflation the International Accounting Standards Board requires corporations to implement financial capital maintenance in units of constant purchasing power in terms of the monthly published Consumer Price Index. This does not result in capital maintenance in units of constant purchasing power since that can only be achieved in terms of a daily index.

A financial asset is a non-physical asset whose value is derived from a contractual claim, such as bank deposits, bonds, and participations in companies' share capital. Financial assets are usually more liquid than other tangible assets, such as commodities or real estate.

A foreign exchange hedge is a method used by companies to eliminate or "hedge" their foreign exchange risk resulting from transactions in foreign currencies. This is done using either the cash flow hedge or the fair value method. The accounting rules for this are addressed by both the International Financial Reporting Standards (IFRS) and by the US Generally Accepted Accounting Principles as well as other national accounting standards.

IAS 39: Financial Instruments: Recognition and Measurement was an international accounting standard which outlined the requirements for the recognition and measurement of financial assets, financial liabilities, and some contracts to buy or sell non-financial items. It was released by the International Accounting Standards Board (IASB) in 2003, and was replaced in 2014 by IFRS 9, which became effective in 2018.

In September 2006, the Financial Accounting Standards Board (FASB) of the United States issued Statement of Financial Accounting Standards 157: Fair Value Measurements), which “defines fair value, establishes a framework for measuring fair value in generally accepted accounting principles (GAAP), and expands disclosures about fair value measurements.” This statement is effective for financial reporting fiscal periods commencing after November 15, 2007 and the interim periods applicable.

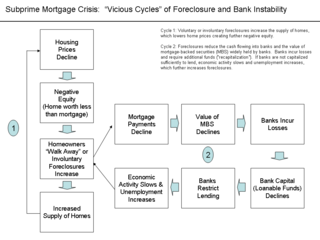

The role of fair value accounting in the subprime mortgage crisis of 2008 is controversial. Fair value accounting was issued as US accounting standard SFAS 157 in 2006 by the privately run Financial Accounting Standards Board (FASB)—delegated by the SEC with the task of establishing financial reporting standards. This required that tradable assets such as mortgage securities be valued according to their current market value rather than their historic cost or some future expected value. When the market for such securities became volatile and collapsed, the resulting loss of value had a major financial effect upon the institutions holding them even if they had no immediate plans to sell them.

International Accounting Standard 16 Property, Plant and Equipment or IAS 16 is an international financial reporting standard adopted by the International Accounting Standards Board (IASB). It concerns accounting for property, plant and equipment, including recognition, determination of their carrying amounts, and the depreciation charges and impairment losses to be recognised in relation to them.

IFRS 9 is an International Financial Reporting Standard (IFRS) published by the International Accounting Standards Board (IASB). It addresses the accounting for financial instruments. It contains three main topics: classification and measurement of financial instruments, impairment of financial assets and hedge accounting. The standard came into force on 1 January 2018, replacing the earlier IFRS for financial instruments, IAS 39.

The accounting profession in Luxembourg is structured around Ordre des Experts-Comptables (OEC) which serves as the main accounting body in the country. Luxembourg accounting standards are inspired from neighbouring France and Belgium. Similar to France, Luxembourg has set up a Commissions des Normes Comptables (CNC) which serves as an advisor to the Ministry for Justice in respect of accounting related matters, e.g. waivers for presenting consolidated accounts.

IAS 14 – Business segments is a former International Accounting Standard that was fully redrawn in 2009 and superseded by IFRS 8. IAS 14 set the guideline on how to identify different business segments of a company.