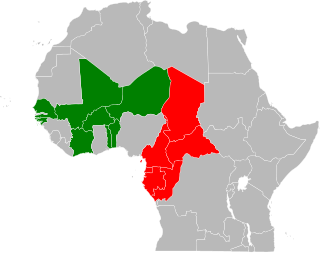

The CFA franc is the name of two currencies, the West African CFA franc, used in eight West African countries, and the Central African CFA franc, used in six Central African countries. Although separate, the two CFA franc currencies have always been at parity and are effectively interchangeable. The ISO currency codes are XAF for the Central African CFA franc and XOF for the West African CFA franc. On 22 December 2019, it was announced that the West African currency would be reformed and replaced by an independent currency to be called Eco.

A currency is a standardization of money in any form, in use or circulation as a medium of exchange, for example banknotes and coins. A more general definition is that a currency is a system of money in common use within a specific environment over time, especially for people in a nation state. Under this definition, the British Pound sterling (£), euros (€), Japanese yen (¥), and U.S. dollars (US$) are examples of (government-issued) fiat currencies. Currencies may act as stores of value and be traded between nations in foreign exchange markets, which determine the relative values of the different currencies. Currencies in this sense are either chosen by users or decreed by governments, and each type has limited boundaries of acceptance; i.e., legal tender laws may require a particular unit of account for payments to government agencies.

A gold standard is a monetary system in which the standard economic unit of account is based on a fixed quantity of gold. The gold standard was the basis for the international monetary system from the 1870s to the early 1920s, and from the late 1920s to 1932 as well as from 1944 until 1971 when the United States unilaterally terminated convertibility of the US dollar to gold, effectively ending the Bretton Woods system. Many states nonetheless hold substantial gold reserves.

In finance, an exchange rate is the rate at which one currency will be exchanged for another currency. Currencies are most commonly national currencies, but may be sub-national as in the case of Hong Kong or supra-national as in the case of the euro.

The Hong Kong dollar is the official currency of the Hong Kong Special Administrative Region. It is subdivided into 100 cents or 1000 mils. The Hong Kong Monetary Authority is the monetary authority of Hong Kong and the Hong Kong dollar.

In international economics, the balance of payments of a country is the difference between all money flowing into the country in a particular period of time and the outflow of money to the rest of the world. These financial transactions are made by individuals, firms and government bodies to compare receipts and payments arising out of trade of goods and services.

The Bretton Woods system of monetary management established the rules for commercial relations among the United States, Canada, Western European countries, and Australia among 44 other countries after the 1944 Bretton Woods Agreement. The Bretton Woods system was the first example of a fully negotiated monetary order intended to govern monetary relations among independent states. The Bretton Woods system required countries to guarantee convertibility of their currencies into U.S. dollars to within 1% of fixed parity rates, with the dollar convertible to gold bullion for foreign governments and central banks at US$35 per troy ounce of fine gold. It also envisioned greater cooperation among countries in order to prevent future competitive devaluations, and thus established the International Monetary Fund (IMF) to monitor exchange rates and lend reserve currencies to nations with balance of payments deficits.

In public finance, a currency board is a monetary authority which is required to maintain a fixed exchange rate with a foreign currency. This policy objective requires the conventional objectives of a central bank to be subordinated to the exchange rate target. In colonial administration, currency boards were popular because of the advantages of printing appropriate denominations for local conditions, and it also benefited the colony with the seigniorage revenue. However, after World War II many independent countries preferred to have central banks and independent currencies.

The foreign exchange market is a global decentralized or over-the-counter (OTC) market for the trading of currencies. This market determines foreign exchange rates for every currency. It includes all aspects of buying, selling and exchanging currencies at current or determined prices. In terms of trading volume, it is by far the largest market in the world, followed by the credit market.

The Mexican peso crisis was a currency crisis sparked by the Mexican government's sudden devaluation of the peso against the U.S. dollar in December 1994, which became one of the first international financial crises ignited by capital flight.

Foreign exchange reserves are cash and other reserve assets such as gold held by a central bank or other monetary authority that are primarily available to balance payments of the country, influence the foreign exchange rate of its currency, and to maintain confidence in financial markets. Reserves are held in one or more reserve currencies, nowadays mostly the United States dollar and to a lesser extent the euro.

The impossible trinity is a concept in international economics and international political economy which states that it is impossible to have all three of the following at the same time:

In macroeconomics and economic policy, a floating exchange rate is a type of exchange rate regime in which a currency's value is allowed to fluctuate in response to foreign exchange market events. A currency that uses a floating exchange rate is known as a floating currency, in contrast to a fixed currency, the value of which is instead specified in terms of material goods, another currency, or a set of currencies.

Revaluation is a change in a price of a good or product, or especially of a currency, in which case it is specifically an official rise of the value of the currency in relation to a foreign currency in a fixed exchange rate system. In contrast, a devaluation is an official reduction in the value of the currency. Under floating exchange rates, a rise in a currency's value is an appreciation. Altering the face value of a currency without changing its purchasing power is a redenomination, not a revaluation.

Currency intervention, also known as foreign exchange market intervention or currency manipulation, is a monetary policy operation. It occurs when a government or central bank buys or sells foreign currency in exchange for its own domestic currency, generally with the intention of influencing the exchange rate and trade policy.

A fixed exchange rate, often called a pegged exchange rate, is a type of exchange rate regime in which a currency's value is fixed or pegged by a monetary authority against the value of another currency, a basket of other currencies, or another measure of value, such as gold.

The London Gold Pool was the pooling of gold reserves by a group of eight central banks in the United States and seven European countries that agreed on 1 November 1961 to cooperate in maintaining the Bretton Woods System of fixed-rate convertible currencies and defending a gold price of US$35 per troy ounce by interventions in the London gold market.

Currency war, also known as competitive devaluations, is a condition in international affairs where countries seek to gain a trade advantage over other countries by causing the exchange rate of their currency to fall in relation to other currencies. As the exchange rate of a country's currency falls, exports become more competitive in other countries, and imports into the country become more and more expensive. Both effects benefit the domestic industry, and thus employment, which receives a boost in demand from both domestic and foreign markets. However, the price increases for import goods are unpopular as they harm citizens' purchasing power; and when all countries adopt a similar strategy, it can lead to a general decline in international trade, harming all countries.

The United States dollar was established as the world's foremost reserve currency by the Bretton Woods Agreement of 1944. It claimed this status from sterling after the devastation of two world wars and the massive spending of the United Kingdom's gold reserves. Despite all links to gold being severed in 1971, the dollar continues to be the world's foremost reserve currency. Furthermore, the Bretton Woods Agreement also set up the global post-war monetary system by setting up rules, institutions and procedures for conducting international trade and accessing the global capital markets using the US dollar.

Fear of floating refers to situations where a country prefers a fixed exchange rate to a floating exchange rate regime. This is more relevant in emerging economies, especially when they suffered from financial crisis in last two decades. In foreign exchange markets of the emerging market economies, there is evidence showing that countries who claim they are floating their currency, are actually reluctant to let the nominal exchange rate fluctuate in response to macroeconomic shocks. In the literature, this is first convincingly documented by Calvo and Reinhart with "fear of floating" as the title of one of their papers in 2000. Since then, this widespread phenomenon of reluctance to adjust exchange rates in emerging markets is usually called "fear of floating". Most of the studies on "fear of floating" are closely related to literature on costs and benefits of different exchange rate regimes.