In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdle rates for businesses, in the form of costs of equity and capital. Since businesses invest that capital in their operations, generally, and in individual projects (or assets), specifically, the big question is whether they generate enough in profits to meet these hurdle rate requirements. In this post, I start by looking at the end game for businesses, and how that choice plays out in investment rules for these businesses, and then examine how much businesses generated in profits in 2023, scaled to both revenues and invested capital.

The End Game in Business

If you start a business, what is your end game? Your answer to that question will determine not just how you approach running the business, but also the details of how you pick investments, choose a financing mix and decide how much to return to shareholders, as dividend or buybacks. While private businesses are often described as profit maximizers, the truth is that if they should be value maximizers. In fact, that objective of value maximization drives every aspect of the business, as can be seen in this big picture perspective in corporate finance:

For some companies, especially mature ones, value and profit maximization may converge, but for most, they will not. Thus, a company with growth potential may be willing to generate less in profits now, or even make losses, to advance its growth prospects. In fact, the biggest critique of the companies that have emerged in this century, many in social media, tech and green energy, is that they have prioritized scaling up and growth so much that they have failed to pay enough attention to their business models and profitability.

For decades, the notion of maximizing value has been central to corporate finance, though there have been disagreements about whether maximizing stock prices would get you the same outcome, since that latter requires assumptions about market efficiency. In the last two decades, though, there are many who have argued that maximizing value and stockholder wealth is far too narrow an objective, for businesses, because it puts shareholders ahead of the other stakeholders in enterprises:

It is the belief that stockholder wealth maximization shortchanges other stakeholders that has given rise to stakeholder wealth maximization, a misguided concept where the end game for businesses is redefined to maximize the interests of all stakeholders. In addition to being impractical, it misses the fact that shareholders are given primacy in businesses because they are the only claim holders that have no contractual claims against the business, accepting residual cash flows, If stakeholder wealth maximization is allowed to play out, it will result in confused corporatism, good for top managers who use stakeholder interests to become accountable to none of the stakeholders:

As you can see, I am not a fan of confused corporatism, arguing that giving a business multiple objectives will mangle decision making, leaving businesses looking like government companies and universities, wasteful entities unsure about their missions. In fact, it is that skepticism that has made me a critic of ESG and sustainability, offshoots of stakeholder wealth maximization, suffering from all of its faults, with greed and messy scoring making them worse.

It may seem odd to you that I am spending so much time defending the centrality of profitability to a business, but it is a sign of how distorted this discussion has become that it is even necessary. In fact, you may find my full-throated defense of generating profits and creating value to be distasteful, but if you are an advocate for the point of view that businesses have broader social purposes, the reality is that for businesses to do good, they have to be financial healthy and profitable. Consequently, you should be just as interested, as I am, in the profitability of companies around the world, albeit for different reasons. My interest is in judging them on their capacity to generate value, and yours would be to see if they are generating enough as surplus so that they can do good for the world.

Profitability: Measures and Scalars

Measuring profitability at a business is messier than you may think, since it is not just enough for a business to make money, but it has to make enough money to justify the capital invested in it. The first step is understanding profitability is recognizing that there are multiple measures of profit, and that each measure they captures a different aspect of a business:

It is worth emphasizing that these profit numbers reflect two influences, both of which can skew the numbers. The first is the

explicit role of accountants in measuring profits implies that inconsistent accounting rules will lead to profits being systematically mis-measured, a point I have made

in my posts on how R&D is routinely mis-categorized by accountants. The other is the

implicit effect of tax laws, since taxes are based upon earnings, creating an incentive to understate earnings or even report losses, on the part of some businesses. That said, global (US) companies collectively generated $5.3 trillion ($1.8 trillion) in net income in 2023, and the pie charts below provide the sector breakdowns for global and US companies:

Notwithstanding their trials and tribulations since 2008, financial service firms (banks, insurance companies, investment banks and brokerage firms) account for the largest slice of the income pie, for both US and global companies, with energy and technology next on the list.

Profit Margins

While aggregate income earned is an important number, it is an inadequate measure of profitability, especially when comparisons across firms, when it is not scaled to something that companies share. As as a first scalar, I look at profits, relative to revenues, which yields margins, with multiple measures, depending upon the profit measure used:

Looking across US and global companies, broken down by sector, I look at profit margins in 2023:

Note that financial service companies are conspicuously absent from the margin list, for a simple reason. Most financial service firms have no revenues, though they have their analogs - loans for banks, insurance premiums for insurance companies etc. Among the sectors, energy stands out, generating the highest margins globally, and the second highest, after technology firms in the United States. Before the sector gets targeted as being excessively profitable, it is also one that is subject to volatility, caused by swings in oil prices; in 2020, the sector was the worst performing on profitability, as oil prices plummeted that year.

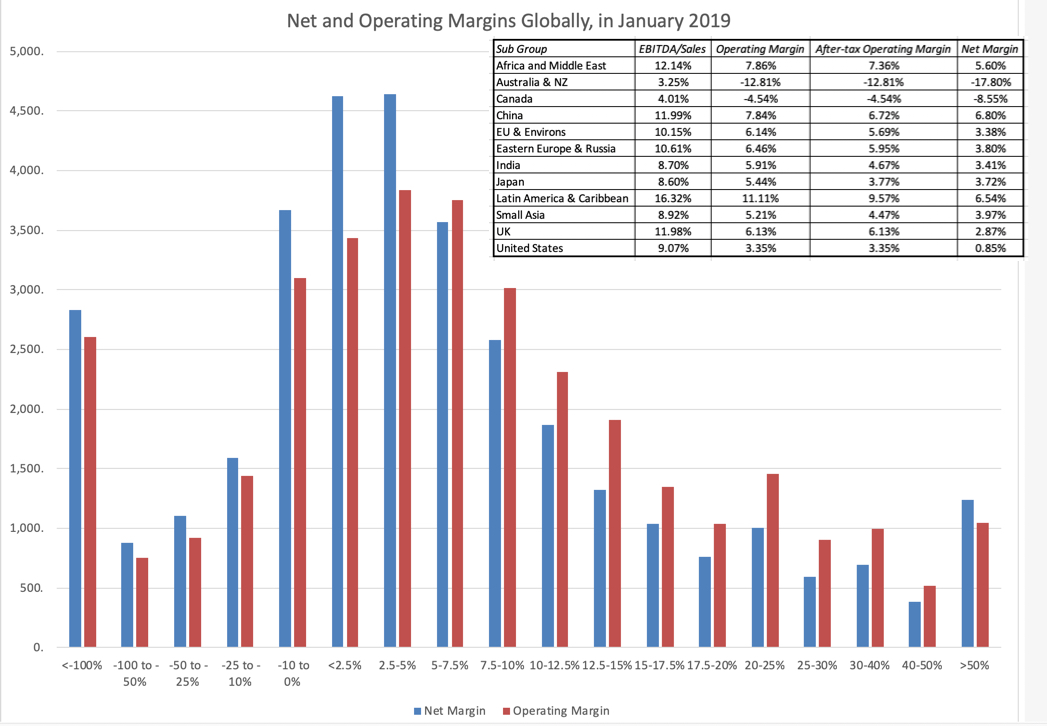

Does profitability vary across the globe? To answer that question, I look at differences in margins across sub-regions of the world:

You may be surprised to see Eastern European and Russian companies with the highest margins in the world, but that can be explained by two phenomena. The first is the preponderance of natural resource companies in this region, and energy companies had a profitable year in 2023. The second is that the sanctions imposed after 2021 on doing business in Russia drove foreign competitors out of the market, leaving the market almost entirely to domestic companies. At the other end of the spectrum, Chinese and Southeast Asian companies have the lowest net margins, highlighting the reality that big markets are not always profitable ones.

Finally, there is a relationship between corporate age and profitability, with younger companies often struggling more to deliver profits, with business models still in flux and no economies of scale. In the fact, the pathway of a company through the life cycle can be seen through the lens of profit margins:

Early in the life cycle, the focus will be on gross margins, partly because there are losses on almost every other earnings measure. As companies enter growth, the focus will shift to operating margins, albeit before taxes, as companies still are sheltered from paying taxes by past losses. In maturity, with debt entering the financing mix, net margins become good measures of profitability, and in decline, as earnings decline and capital expenditures ease, EBITDA margins dominate. In the table below, I look at global companies, broken down into decals, based upon corporate age, and compute profit margins across the deciles:

The youngest companies hold their own on gross and EBITDA margins, but they drop off as you move to operating nnd net margins.

In summary, profit margins are a useful measure of profitability, but they vary across sectors for many reasons, and you can have great companies with low margins and below-average companies that have higher margins. Costco has sub-par operating margins, barely hitting 5%, but makes up for it with high sales volume, whereas there are luxury retailers with two or three times higher margins that struggle to create value.

Return on Investment

The second scalar for profits is the capital invested in the assets that generate these profits. Here again, there are two paths to measuring returns on investment, and the best way to differentiate them is to think of them in the context of a financial balance sheet:

The accounting return on equity is computed by dividing the net income, the equity investor's income measure, by the book value of equity and the return on invested capital is computed, relative to the book value of invested capital, the cumulative values of book values of equity and debt, with cash netted out. Looking at accounting returns, broken down by sector, for US and global companies, here is what 2023 delivered:

In both the US and globally, technology companies deliver the highest accounting returns, but these returns are skewed by the accounting inconsistencies in capitalizing R&D expenses. While I partially correct for this by capitalizing R&D expenses, it is only a partial correction, and the returns are still overstated. The worst accounting returns are delivered by real estate companies, though they too are skewed by tax considerations, with expensing to reduce taxes paid, rather than getting earnings right.

Excess Returns

In the final assessment, I bring together the costs of equity and capital estimated in the last post and the accounting returns in this one, to answer a critical question that every business faces, i.e,, whether the returns earned on its investment exceed its hurdle rate. As with the measurement of returns, excess returns require consistent comparisons, with accounting returns on equity compared to costs of equity, and returns on capital to costs of capital:

These excess returns are not perfect or precise, by any stretch of the imagination, with mistakes made in assessing risk parameters (betas and ratings) causing errors in the cost of capital and accounting choices and inconsistencies affecting accounting returns. That said, they remain noisy estimates of a company's competitive advantages and moats, with strong moats going with positive excess returns, no moats translating into excess returns close to zero and bad businesses generating negative excess returns.

I start again by looking at the sector breakdown, both US and global, of excess returns in 2023, in the table below:

In computing excess returns, I did add a qualifier, which is that I would do the comparison only among money making companies; after all, money losing companies will have accounting returns that are negative and less than hurdle rates. With each sector, to assess profitability, you have to look at the percentage of companies that make money and then at the percent of these money making firms that earn more than the hurdle rate. With financial service firms, where only the return on equity is meaningful, 57% (64%) of US (global) firms have positive net income, and of these firms, 82% (60%) generated returns on equity that exceeded their cost of equity. In contrast, with health care firms, only 13% (35%) of US (global) firms have positive net income, and about 68% (53%) of these firms earn returns on equity that exceed the cost of equity.

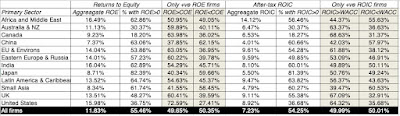

In a final cut, I looked at excess returns by region of the world, again looking at only money-making companies in each region:

To assess the profitability of companies in each region, I again look at t the percent of companies that are money-making, and then at the percent of these money-making companies that generate accounting returns that exceed the cost of capital. To provide an example, 82% of Japanese companies make money, the highest percentage of money-makers in the world, but only 40% of these money-making companies earn returns that exceed the hurdle rate, second only to China on that statistic. The US has the highest percentage (73%) of money-making companies that generate returns on equity that exceed their hurdle rates, but only 37% of US companies have positive net income. Australian and Canadian companies stand out again, in terms of percentages of companies that are money losers, and out of curiosity, I did take a closer look at the individual companies in these markets. It turns out that the money-losing is endemic among smaller publicly traded companies in these markets, with many operating in materials and mining, and the losses reflect both company health and life cycle, as well as the tax code (which allows generous depreciation of assets). In fact, the largest companies in Australia and Canada deliver enough profits to carry the aggregated accounting returns (estimated by dividing the total earnings across all companies by the total invested capital) to respectable levels.

In the most sobering statistic, if you aggregate money-losers with the companies that earn less than their hurdle rates, as you should, there is not a single sector or region of the world, where a majority of firms earn more than their hurdle rates.

In 2023, close to 80% of all firms globally earned returns on capital that lagged their costs of capital. Creating value is clearly far more difficult in practice than on paper or in case studies!

A Wrap!

I started this post by talking about the end game in business, arguing for profitability as a starting point and value as the end goal. The critics of that view, who want to expand the end game to include more stakeholders and a broader mission (ESG, Sustainability) seem to be operating on the presumption that shareholders are getting a much larger slice of the pie than they deserve. That may be true, if you look at the biggest winners in the economy and markets, but in the aggregate, the game of business has only become harder to play over time, as globalization has left companies scrabbling to earn their costs of capital. In fact, a decade of low interest rates and inflation have only made things worse, by making risk capital accessible to young companies, eager to disrupt the status quo.

YouTube Video

Datasets

- Profit Margins, by Industry (US, Global)

- Accounting Returns and Excess Returns, by Industry (US, Global)

Data Update Posts for 2024