The conceptual framework for financial reporting

•Download as PPTX, PDF•

3 likes•4,693 views

The Conceptual Framework for Financial Reporting (IFRS Framework) establishes the fundamental concepts for preparing financial statements according to IFRS. It describes the basic principles and guidance for presentation, recognizes that it underwent name changes and updates over time, and is not a standard itself but provides important guidance. The IFRS Framework consists of 4 chapters that cover the objectives of general purpose financial reporting, the reporting entity, qualitative characteristics of useful financial information, and the remaining text from the 1989 framework.

The conceptual framework for financial reporting

- 1. *

- 2. The Conceptual Framework for the Financial Reporting (IFRS Framework) serves as a pillar on which the whole IFRS stand. • It describes the basic principles for presentation and preparation of financial statements in line with IFRS. • a “must-read” document prior to any other IFRS or IAS standard. The IFRS Framework underwent certain changes over past years. • Previously called “Framework for the Preparation and Presentation of Financial Statements”. • Last update happened in September 2010, … please check our MFRS The IFRS Framework itself is not a standard, but it is important - gives the users guidance of how the financial statements shall be prepared. IFRS Framework consists of 4 chapters Source: www.IFRSbox.com

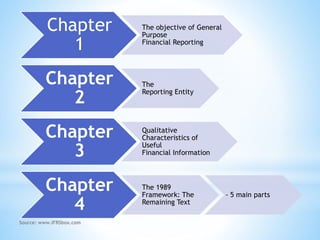

- 3. Chapter 1 Source: www.IFRSbox.com The objective of General Purpose Financial Reporting Chapter 2 The Reporting Entity Chapter 3 Qualitative Characteristics of Useful Financial Information Chapter 4 The 1989 Framework: The Remaining Text - 5 main parts

- 4. ASSUMPTIONS 1. Economic entity 2. Going concern 3. Monetary unit 4. Periodicity 5. Accrual PRINCIPLES 1. Measurement 2. Revenue recognition 3. Expense recognition 4. Full disclosure CONSTRAINTS 1. Cost 2. Materiality ELEMENTS 1. Assets 2. Liabilities 3. Equity 4. Income 5. Expenses OBJECTIVE Provide information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in their capacity as capital Providers. Second level First level Third level QUALITATIVE CHARACTERIS TICS 1. Fundamen tal qualities 2. Enhancing qualities