The Best Home-Buying Checklist: From First Tour to Final Closing

Keep the stress of buying a new home from taking away from the excitement with this easy-to-use home buying checklist

If you’re shopping for a new home, you’re going to have a lot of things to remember. You’ll need to keep track of important paperwork for your lender, be sure you have the contact information on hand for a laundry list of real estate professionals (your real estate agent, a home inspector, and maybe even a lawyer, depending on where you live), as well as remembering details about every house you see. Keeping all of this organized while also shopping for your dream home can end up feeling like a second job.

Utilizing a home buying checklist will help keep everything you need to know at your fingertips until you’re finally holding the keys to your new home.

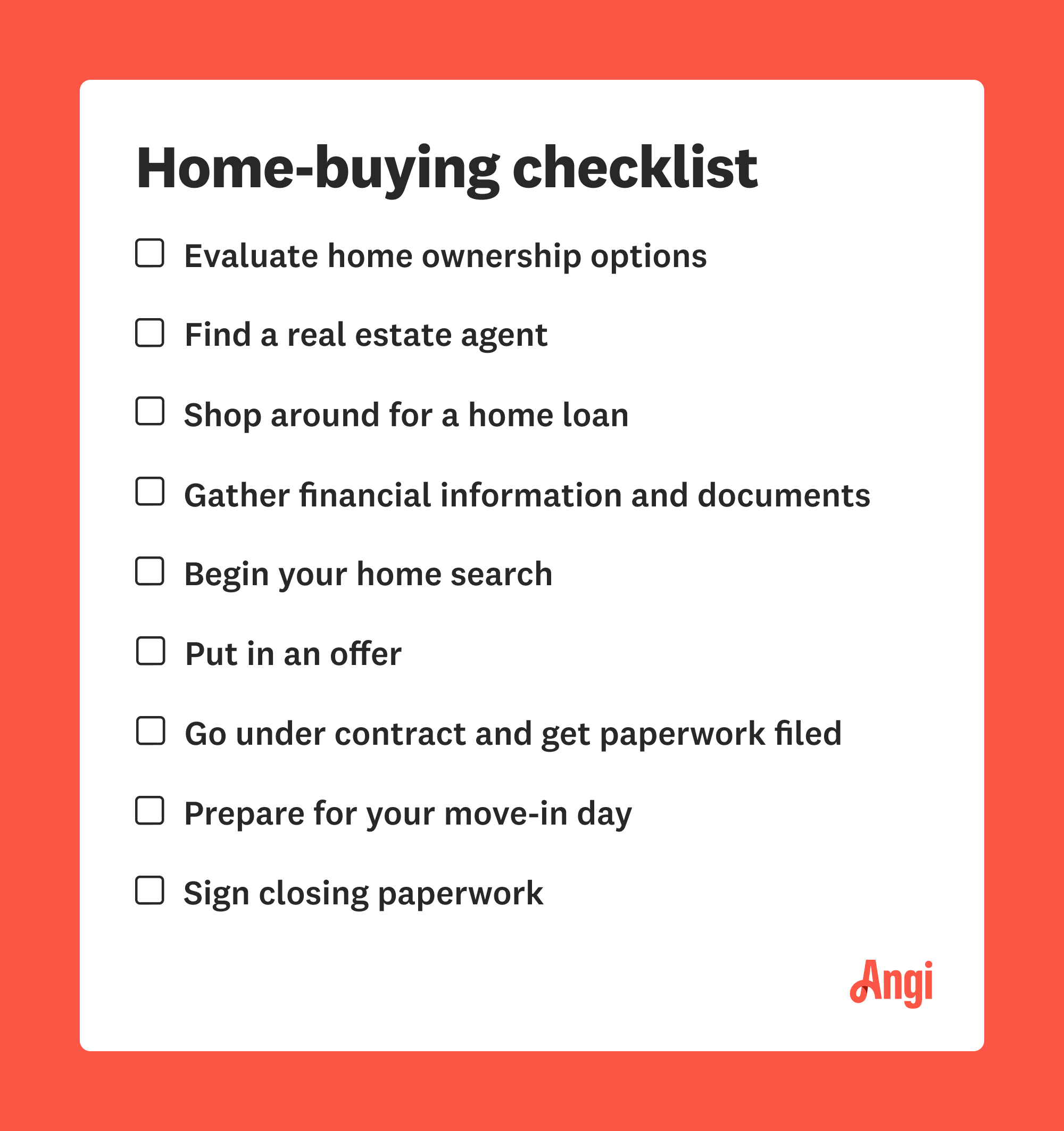

1. Are You Ready for Homeownership?

Before you even download your first real estate app, you should take a good look at your budget and see if you’re financially ready to purchase. Things you’ll need to look at:

Your debt-to-income ratio: This is something lenders will consider by taking the amount of debt you pay each month (like auto loans, student loans, and credit cards) and dividing it by your gross monthly income (the money you pay before taxes). The lower this number, the better shape you’ll be in when it comes to getting a mortgage.

Your savings: Some loan programs offer 100% financing, while others require you to bring at least 20% of the purchase price of your home to the table. Do you have enough saved up for a down payment?

Financial responsibility: Owning a home is a huge investment that stretches way beyond the monthly mortgage payment. You’ll need to be ready to deal with things like routine maintenance, lawn care, and even the occasional paint job.

2. Find a Real Estate Agent

If you’re ready to move forward with buying a home, you should find a real estate agent who focuses on the geographical area where you want to live. They will have the best recommendations for other real estate pros that you’ll need down the line, and they’ll also have a good idea of who you should call for a pre-approval.

Your realtor will be by your side throughout this process, so you’ll want to make sure you’re teaming up with a real estate agent who gets what you’re looking for and your preferred communication style. For example, don’t team up with a realtor who prefers to talk on the phone when you’re strictly a text message kind of communicator.

3. Shop Around for a Home Loan

There are a lot of things you’ll want to consider before moving forward with a lender. One of the big things is whether or not they handle the types of loan programs you want to use. Remember those loans that require 0% down? If that’s the route you want to go, you’ll need to make sure that you’re using a licensed lender in those specialized programs, which is called a USDA Mortgage.

Additionally, you’ll want to make sure you’re getting the best deal. Look at the interest rates offered by a lender, as well as the Annual Percentage Rate (or APR). While your APR is expressed as an interest rate, it’s actually a figure that combines the entire cost of your loan, including fees and closing costs, to give you a clearer picture of how much mortgages from different lenders would actually cost you over the life of your loan.

4. Gather Your Documents

Once you finally find a lender, it’s going to feel like they want to see every financial document you’ve ever received. Some of the core documents you’ll need for your pre-approval can include:

Two years of W2s

Two most recent pay stubs

Two months to six months of bank statements

Your previous year’s tax returns

Explanation letters for anything unusual on your credit report

5. Start Your Home Search

It doesn’t matter if you already have a dream home in mind or if you have no idea what you’re looking for, as long as you can come up with a few criteria to give your real estate agent. Once you receive your pre-approval from your lender (which will tell you how much purchasing power you have), that will help guide you both in the search. Some important things to consider are the details that will be hard (or impossible) for you to change once you’ve moved in.

The school district

The number of bathrooms

If you will want one-floor living

How you feel about living on a busy street

6. Putting in an Offer

After you’ve found your dream home, you and your realtor will work together on drafting an offer letter. This document will tell the sellers how much you’re willing to pay, including how much of a down payment you’re comfortable with, what type of mortgage program you’ll be using, and any contingencies you may be holding out for (like whether you’ll still be interested in buying the property if a home inspection reveals a problem). Before signing your offer letter, you should consider the following things:

How close to your approved loan amount do you want to go?

What contingencies (if any) are you willing to waive?

How soon do you want to close?

Will you be open to a counteroffer if the seller rejects your initial offer?

Have you done your due diligence on the new property and checked for things like plumbing issues, prior damage, moisture issues, or the electrical panel? All of these things can turn into big expenses down the line.

7. Going Under Contract

Being “under contact” on your future home is a dream come true for most people. It’s also when the bulk of the real work begins. You’ll likely have to provide additional documents to your lender as part of the final approval process and call around to schedule all sorts of inspections and appointments.

Here are a few of the things you’ll need to make sure you’re doing at this point:

Responding to your lender’s ongoing document requests

Writing down any timelines for your contract (you may only have a certain number of days for items like your appraisal, inspection, and to act on any contingencies)

Paying for the appraisal

Talking to the title company or real estate attorney handling the escrow process

8. Preparing to Move

While all of this is going on in the background, you’ll also need to be preparing for your move. This means packing up your current home, contacting your utility companies, and gathering the documents you’ll need to change your address. Some things you’ll need to do:

Contact your current utility providers (like electric, water, and internet service providers) to let them know which date you’ll need your service shut off at your old location and turned on at your new location.

Contact utility providers for features you didn’t have at your old place (if you rented, for instance, you might not have had a water bill in your name).

Contact the postal service to have your mail forwarded to your new address until you’ve had a chance to update your address with anyone who may be sending you correspondence.

Get the forms needed to change your address on government or state documents like your driver’s license or car registration.

Price out moving companies and rental trucks (or buttering up your friend with a pickup truck) to make sure you have the heavy lifting covered on moving day.

Schedule your closing date.

9. Signing on the Dotted Line

Once the big day has finally arrived and you’re finally ready to sign the closing paperwork and get the keys to your new home, you’ll need to make sure you have everything the title company needs to complete the closing. These items can include, but aren’t limited to:

An official photo ID

A certified check, money order, or wire information for any money that you still owe at closing

An hour or two of free time so that you don’t feel rushed when looking through your closing documents before signing them

A keychain to clip your new keys onto because, congratulations, you just bought a house